If you want to build a fintech app in 2026, here’s the thing: you’re going to need more than coding knowledge. You also need to understand the industry, know your users, and stay on top of the latest tech. Today’s users are digitally savvy, and they’re expanding their tech expectations to things like biometric logins and embedded payments. All of this new and exciting tech also comes with increased compliance requirements.

The solutions we build at Aloa are developed with those considerations in mind. Our projects are grounded in a clear understanding of your business goals. This helps us quickly validate ideas with rapid prototyping and scale confidently once we’ve built the right foundation. We’re also continuously testing, learning, and refining our approach, applying our insights directly to the solutions we build.

In this blog, I’ll tell you exactly how to build a fintech app tailored to the market trends of 2026. I’ll go over essential features and explore the top market trends that should inform your design decisions.

Let's get started!

TL;DR

- Every successful app starts with a well-defined strategy. Validate your idea through market research, competitor analysis, and a clear unique value proposition before writing a single line of code.

- Regulations like GDPR and PSD2 need to be baked into the code from day one. This saves you from having to deal with layering on compliance after the core features have already been built.

- Clean UX goes a long way. Seamless transactions and responsive design are huge trust drivers. Faster apps beat slower apps, even though the slower app might be more feature-rich.

- With the right tech stack, you can adapt to user needs and keep growing without having to rebuild from scratch. Scalable, secure technologies like modern front-end frameworks and strong back-end architecture are critical foundations for this. Adding the right amount of cloud infrastructure into the mix helps you stay agile.

- Test, launch, improve. Rigorous testing and continuous iteration based on user feedback is how you turn an idea into a real, usable product.

How to Build a FinTech App in 2026

To build a fintech app in 2026, you’ll need a strategic blend of industry insight, technical skills, and a keen eye on emerging trends. Let’s walk through the essential steps to put those three principles into practice.

Step 1: Market Research and Ideation

Market research and ideation are a pivotal first step in building a successful FinTech app. This process lays the groundwork for developing a product that fills a market gap and resonates with your target audience. Here's how to approach it:

- Identify Your Niche: Delve into the FinTech sector to find areas ripe for innovation. Whether it's personal finance, payments, trading, or lending, select a niche where you can make a significant impact.

- Analyze Competitors: Examine top FinTech apps, noting their strengths and weaknesses. Tools like SWOT analysis can provide insights into where competitors excel and where there are opportunities for differentiation.

- Understand User Needs: Conduct surveys, interviews, and focus groups to gather information on potential users' preferences, pain points, and desired features. This feedback is invaluable for tailoring your app's functionality and user experience.

- Spot Market Gaps: Look for unmet needs within your chosen niche. For instance, users may want better tools for managing outstanding balances, tracking repayments, or automatically identifying opportunities for debt consolidation to reduce financial stress.

- Craft Your Value Proposition: Define what makes your app different and better based on your research. This unique value proposition (UVP) should clearly articulate your app's benefits to users.

Taking these steps ensures that your FinTech app is built on a solid foundation of market understanding and user-centric design, setting the stage for its future success.

Step 2: Regulatory Compliance and Security

Navigating the complex regulatory landscape is paramount in developing a FinTech app. Understanding legal requirements and compliance standards across your target markets is non-negotiable. Early implementation of robust security measures, such as data encryption and secure authentication methods, is essential to safeguard user data and build trust. Adherence to specific regulations, like the General Data Protection Regulation (GDPR) in Europe or the Payment Services Directive (PSD2), ensures your app meets the highest privacy and security standards.

This proactive approach to regulatory compliance and security minimizes the risk of legal complications and positions your app as a reliable and secure choice for users. Tailoring your compliance strategy to the nuances of each geographical market, while aligning with SOC 2 compliance requirements where applicable, enhances your app’s global appeal and supports a consistent, secure user experience across borders.

Step 3: Design and User Experience (UX)

Designing a user-friendly interface is paramount in creating a FinTech app, where simplicity and ease of use are crucial to ensuring a positive user experience (UX). An intuitive UX design facilitates seamless financial transactions and navigation and drives user adoption and satisfaction. Here's a brief breakdown of essential elements to consider:

.webp)

- Intuitive Navigation: Ensure that users can easily find what they're looking for without unnecessary clicks or confusion. Simplify the journey to the most critical tasks, such as checking balances, making payments, or viewing transaction histories.

- Simplified Transactions: Design the transaction process to be straightforward, minimizing the steps needed to complete an action. Clarity in transaction forms, confirmation messages, and error notifications enhances user confidence.

- Responsive Design: The app should offer a consistent experience across various devices and screen sizes, ensuring functionality and readability on smartphones, tablets, and desktops.

- Accessibility: Incorporate accessibility features to accommodate all users, including those with disabilities. This includes text readability, voice commands, and easy navigation for a wider audience.

- Visual Clarity: Use clear, visually appealing design elements that align with your brand. Adequate spacing, contrasting colors for essential actions, and minimalistic design can make the app more engaging and less overwhelming.

A well-executed UX design in your FinTech app not only meets the functional needs of users but also fosters trust and loyalty, setting the foundation for long-term success in the competitive FinTech landscape.

Step 4: Technology Stack and Development

Selecting the appropriate technology stack is crucial in developing a FinTech app, as it underpins its performance, scalability, and security. Opt for technologies known for robustness and agility, such as React for front-end development, Node.js for the back-end, and cloud services like AWS for scalable infrastructure. Utilizing agile development methodologies facilitates flexible and iterative design, enabling your team to swiftly adapt to changes and refine the app based on user feedback and testing outcomes.

Partnering with an expert development company like Aloa can be a game-changer. Aloa’s expertise in building high-quality, secure, and scalable FinTech applications ensures that your app meets and exceeds industry standards. With Aloa, you can confidently navigate the intricacies of FinTech app development, from choosing the right technology stack to successfully launching your app.

Step 5: Testing and Quality Assurance

Testing and quality assurance in FinTech app development are critical phases that must be considered. Ensuring the app’s functionality, security, and performance adhere to the highest standards demands a comprehensive testing strategy. Here's a brief overview of the essential testing types each FinTech app must undergo:

- Unit Testing: Validate each component or module works correctly in isolation, ensuring reliability in the app's most minor functional pieces.

- Integration Testing: Assess how well different modules or services work together, highlighting issues in the interaction between components.

- Security Testing: Crucial for FinTech applications, this testing identifies vulnerabilities and ensures data protection, encryption, and compliance with financial regulations.

- Performance Testing: Evaluate the app’s speed, responsiveness, and stability under various conditions, ensuring it can handle high volumes of transactions and users.

- User Acceptance Testing (UAT): Conducted with real users to ensure the app meets their needs and expectations, providing user experience and functionality feedback.

By meticulously conducting these tests, developers can identify and rectify any issues, ensuring the FinTech app is robust, secure, and user-friendly upon launch. This rigorous approach to quality assurance is essential for building trust and ensuring the app's long-term success in the competitive FinTech.

Step 6: Launch and Continuous Improvement

Launching your FinTech app begins a journey towards achieving and maintaining success in the competitive FinTech market. Here’s how to ensure continuous improvement:

- Gather User Feedback: Actively seek and listen to user feedback through surveys, app reviews, and social media. This insight is invaluable for identifying areas for enhancement and new features that users desire.

- Monitor Performance Metrics: Utilize analytics tools to track app performance, user engagement, and retention rates. Key metrics can guide decisions on where to allocate resources for improvements.

- Stay Updated with FinTech Trends: The FinTech industry is rapidly evolving. Keep abreast of the latest trends and technologies to ensure your app remains relevant and innovative.

- Iterate and Evolve Your App: Implement an agile development process, allowing regular updates and iterations based on user feedback and emerging market needs.

- Scale Marketing Efforts: As your app matures, adjust and scale your marketing strategies to attract new users while retaining existing ones. Tailored campaigns, referral programs, and promotional offers can be effective tools.

By focusing on these areas, you can ensure that your FinTech app not only stays ahead of the curve but also continuously improves to meet your user base's changing needs and preferences.

Features of a FinTech App

The FinTech sector continues to revolutionize how people manage their finances, from mobile banking to investment options, reshaping personal finance with innovative technologies. Understanding the top features that set a successful FinTech app apart is crucial for anyone looking to hire FinTech application developers.

Admin Side Features of FinTech Applications

On the admin side, features are designed to provide control and oversight, ensuring that the app runs smoothly and securely. Here are ten critical admin features:

- Dashboard Analytics: For real-time monitoring of user activities, transaction volumes, and app performance, helping financial advisors and app administrators make informed decisions.

- User Management: Enables administrators to manage user accounts, including activations, suspensions, and permission settings.

- Transaction Monitoring: Essential for tracking all user transactions, spotting unusual activity, and managing commission fees effectively.

- Security Controls: Includes encryption, fraud detection mechanisms, and secure access controls to protect user data and transactions.

- Compliance Tools: Ensures the app meets all regulatory requirements, a vital aspect of the FinTech industry.

- Payment Processing: Admin tools for managing direct deposits, cash advances, and payment settlements.

- Customer Support Module: Provides admins with tools to offer support, manage queries, and resolve issues efficiently.

- Financial Reporting: Generates detailed reports on financial performance, including earnings, withdrawals, and commission fees. Many fintech platforms also integrate with the best financial reporting software to generate deeper financial insights and improve decision-making.

- Marketing Tools: For running and managing promotional campaigns, targeting users based on their behavior and preferences.

- Feedback Collection: Enables admins to gather user feedback directly within the app, facilitating continuous improvement.

User Side Features of FinTech Applications

A FinTech app must be intuitive, secure, and feature-rich for users, catering to various financial needs. Here are ten essential user-side features:

- Account Management: Allows users to easily manage their bank accounts, credit cards, and investment portfolios in one place.

- Payment Options: Supports various payment methods, including credit/debit card transactions, mobile payments like PayPal and Venmo, and cryptocurrencies through platforms like Coinbase.

- Personal Finance Tools: Features like budgeting, expense tracking, and financial planning help users manage their finances effectively.

- Investment Opportunities: Offers access to various investment options, including stocks, ETFs, and cryptocurrencies, with apps like Robinhood and Acorns leading the way.

- Loan and Credit Management: Helps users manage loans, consolidate credit card debt, understand their credit score, and explore options for improving it.

- Savings and Rewards: Encourages saving through features like automatic spare change investments and rewards like cashback and Nubank reward points.

- Security Features: Protects user data with encryption, secure login mechanisms, and real-time transaction notifications.

- Customizable Alerts: Tell users about their account balances, stock market movements, and upcoming bills or payments.

- Educational Resources: Offers a range of educational resources and tips on personal finance, trading, and investment strategies.

- User Experience: Prioritizes a seamless, intuitive user experience across all mobile devices, ensuring easy navigation and access to features.

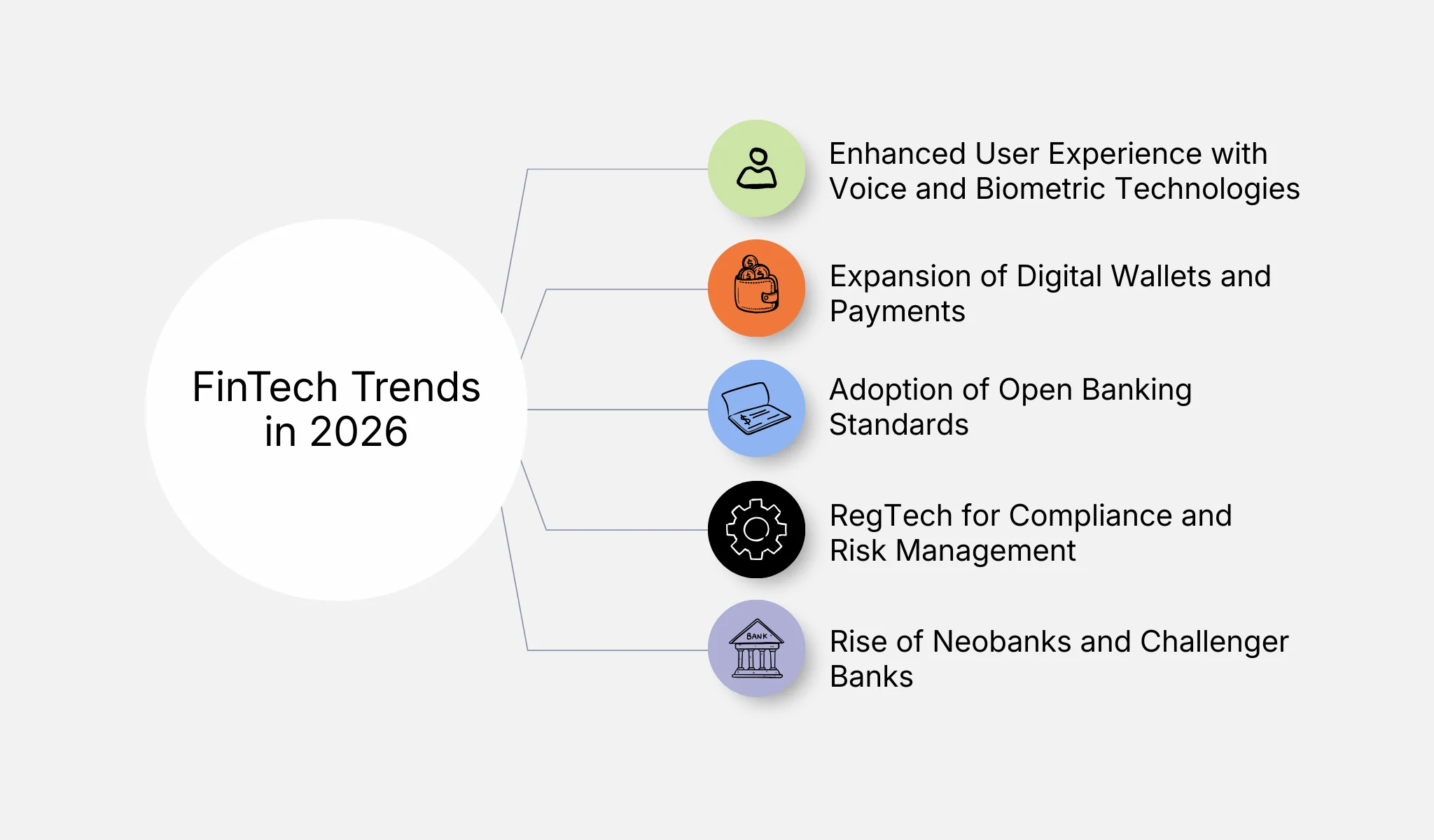

FinTech Trends in 2026 to Watch For

The FinTech app landscape constantly evolves, driven by technological advancements, regulatory changes, and shifting consumer behaviors. As we move into 2026, several key trends are set to shape the development, functionality, and adoption of FinTech applications. Here are five significant trends to watch:

Enhanced User Experience with Voice and Biometric Technologies

In 2026, the FinTech industry will elevate user experiences by integrating voice and biometric technologies into FinTech apps. This trend caters to the growing demand for seamless, secure access to financial services, making it essential for top FinTech applications looking to enhance security and user convenience.

By adopting these technologies, FinTech companies can offer personalized access to services directly through mobile apps, from checking accounts to trading platforms. However, implementing voice and biometric technologies requires careful consideration of privacy concerns and data security, ensuring that users' biometric data are handled with the utmost integrity and transparency.

Expansion of Digital Wallets and Payments

In 2026, the FinTech industry is witnessing a significant expansion of digital wallets and payments, a trend driven by the increasing demand for contactless transactions and the global shift towards cashless societies. Digital wallets streamline the payment process and integrate other financial services, making them a versatile tool for users.

Adopting this trend by FinTech applications allows for a more efficient, secure, and convenient transaction experience. However, implementing digital wallets and payments requires careful attention to security measures, regulatory compliance, and user interface design to ensure a seamless and safe user experience.

Adoption of Open Banking Standards

Adopting open banking standards is revolutionizing the FinTech industry in 2026, shifting towards more transparent, accessible, and collaborative financial ecosystems. Open banking enables third-party developers to create apps and services around financial institutions, facilitating the sharing of financial information more securely and efficiently with the customer's consent.

This trend is being embraced for its potential to enhance customer experiences, offer personalized financial services, and promote innovation within the sector. However, implementing open banking standards necessitates rigorous data protection measures, adherence to regulatory requirements, and the establishment of secure API frameworks to protect sensitive customer information.

RegTech for Compliance and Risk Management

The finTech industry increasingly turns to Regulatory Technology (RegTech) for compliance and risk management solutions. RegTech utilizes advanced technologies such as AI in FinTech, machine learning, and blockchain to streamline and automate compliance processes for financial institutions. This trend is critical in an era where regulatory requirements are becoming more complex and stringent across global markets.

By adopting RegTech, FinTech companies can enhance their compliance posture, reduce operational risks, and improve efficiency. However, implementing RegTech requires a deep understanding of the regulatory landscape, integration with existing systems, and ongoing monitoring to adapt to new regulations effectively.

Rise of Neobanks and Challenger Banks

The rise of neobanks and challenger banks marks a pivotal trend in the FinTech industry in 2026, as these digital-first financial institutions continue to disrupt traditional banking with innovative approaches. Unlike conventional banks, neobanks operate exclusively online or via mobile apps, offering a range of financial services that are typically faster, more user-friendly, and less costly.

This shift reflects consumer demand for more accessible, transparent, personalized banking experiences. The adoption of this trend is fueled by advancements in technology, changing consumer behaviors, and a regulatory environment that supports financial innovation. However, for neobanks and challenger banks to thrive, they must prioritize robust security measures, ensure regulatory compliance, and continuously innovate to meet evolving customer expectations.

Key Takeaway

Like everything AI touches, the fintech industry got a massive overhaul in recent years. Yesterday’s frontier tech is becoming today’s standard, but not everyone is adopting at the same pace. This uniquely positions those who want to build a fintech app to address current customer expectations ahead of everyone else.

Like any digital product, a fintech app isn’t a one-and-done deal. You’ve got to keep iterating and improving. Do that right, and your app can not only meet today’s needs, but also be ready for whatever comes next.

Constant improvement is our mantra here at Aloa. Every innovation is published in our case studies and technical deep-dives, advancing AI education for all and helping us ensure each solution builds on what the previous one did right and fixes what it did wrong. If you’d like to build a fintech app with us, chat with us today. We’re excited to hear your ideas!

If you’d like to read more on fintech and other AI sectors, check out the rest of our blog. We also have an active Discord server full of fantastic AI builders like you and me, constantly sharing ideas back and forth. If newsletters are more your speed, take a look at Byte-Sized. Compiled by my co-founder David Pawlan, Byte-Sized brings you the latest developments in AI and advanced tech over the past 24 hours.

FAQs

What are effective strategies for conducting market research in the fintech industry?

Effective market research combines the following:

- Surveys and interviews: Direct feedback from your target audience helps you understand their preferences, pain points, and expectations.

- Social media listening and competitor analysis: Monitor social platforms and track competitor activity to uncover trends, sentiment, and gaps in the market.

- Data analytics: Quantitative data from user behavior, transactions, and other sources help validate assumptions and optimize your product for maximum impact.

All of these strategies help you identify opportunities and position your offerings strategically.

How can fintech startups leverage AI to enhance user experience?

AI brings powerful benefits to UX thanks to things like NLP and machine learning, such as:

- Personalized financial recommendations: AI analyzes user behavior, transaction history, and goals to tailor everything from self-assistance to budgeting and investment tips.

- Automated customer support: AI-powered chatbots and virtual assistants provide 24/7 support, ensuring customer concerns always get addressed.

- Predictive fraud alerts: Machine learning models detect unusual activity in real-time, allowing fraud detection systems to warn users ahead of time about suspicious activity.

What are key considerations when selecting a payment gateway for a fintech app?

The main factors you should account for are:

- Transaction fees

- Supported currencies

- Security features

- Ease of integration with your current stack

How can fintech apps improve user retention and engagement?

Retention begins with intuitive onboarding. Once you’ve got that down, you can maximize user engagement with rewards programs, personalized journeys, and continuous feature updates based on feedback.

These are principles we apply throughout the fintech solutions we build at Aloa. We make full use of foundational NLP models like FinLlama and InvestLM to deliver context-aware financial insights and personalized recommendations.

What are potential challenges in integrating blockchain into a fintech app?

Blockchain offers some groundbreaking security and transparency benefits, but it also creates challenges like:

- Regulatory complexity: Blockchain makes cross-border payments much easier, but that also means they operate across several jurisdictions. Each one can have different regulations around data privacy and security.

- Scalability limitations: Public blockchains can face network congestion, slowing down transactions and causing gas fees to fluctuate.

- Technical integration challenges: Integrating blockchain with legacy systems requires specialized expertise.

Aloa’s fintech blockchain services can help you navigate these complexities while aligning the new tech with your business objectives. We have experience in helping legacy institutions adopt blockchain without interrupting their daily workflows, even those with aging tech stacks.