Way before AI started reshaping tech as a whole, the fintech industry was already modernizing the financial services sector with digital payments, mobile banking, peer-to-peer lending, and more. Now that AI, blockchain, and big data are here, fintech innovation has only gotten faster. All of these new technologies working together make financial services smarter, more secure, and more accessible than ever before.

At Aloa, we are at the forefront of AI in fintech. Each solution we develop begins from a deep understanding of each client’s goals and challenges. This lets us customize every feature to integrate smoothly with your existing operations. We’re also committed to advancing the field of AI, publishing our innovations in the form of case studies, technical deep-dives, and industry insights such as this article.

In this blog, we’ll take an in-depth look at what fintech is, how it works, the challenges it faces, and the different sectors it touches.

TL;DR

- What is fintech industry? Fintech stands for “financial tech” and is meant to improve accessibility, efficiency, personalization, and scalability across the entire financial ecosystem.

- Fintech spans several core sectors, including banking, payments, lending, investing, insurance (insurtech), and regulatory technology (regtech).

- Fintech software makes financial services better through automation, advanced analytics, seamless integrations (APIs, open banking), and user-centric digital experiences.

- Common fintech software types include mobile banking apps, payment processors, trading platforms, robo-advisors, and compliance/risk tools.

What is Fintech?

Fintech just means “financial tech”, but it goes much deeper than just payment processing and accessing your bank account on your phone. The fintech industry enables things like real-time fraud detection, automated credit risk assessment, and integrating financial services into everyday digital platforms.

At its core, fintech is all about using technology to make financial services work better for users and easier to provide for companies.

Fintech Sectors

Fintech encompasses a wide range of sectors, each contributing to the transformation of the finance industry. From banking and payments to lending, investment, insurance, and regulatory technology, fintech is reshaping how we engage with financial services.

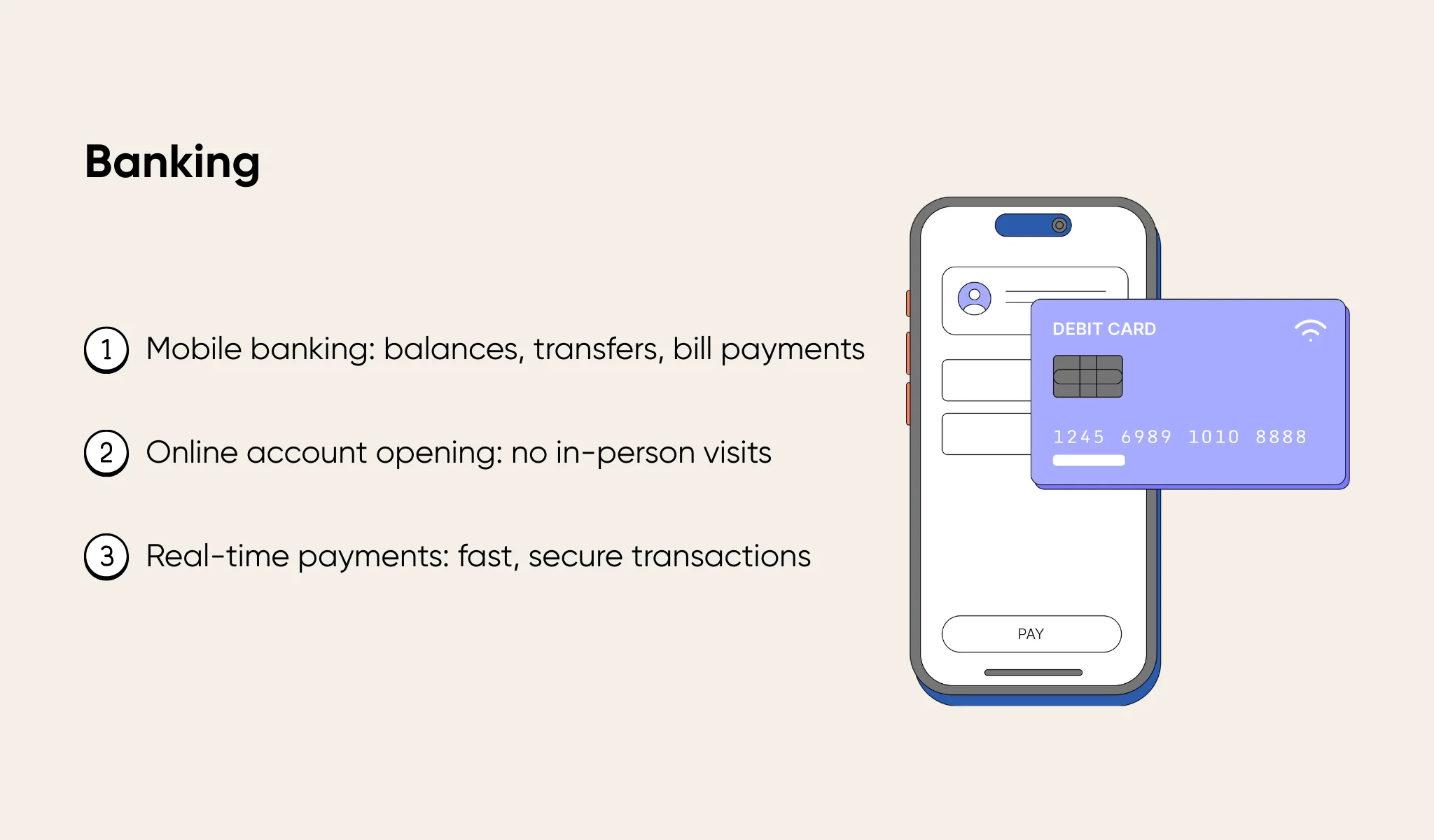

Banking

In the realm of banking, fintech has ushered in significant changes. Traditional banks, challenger banks, and neobanks have embarked on digital transformations to enhance their services and remain competitive in the digital age.

Brief Overview

Challenger banks and neobanks, characterized by their digital-first approach, have emerged as formidable competitors to traditional banks. They prioritize user-friendly interfaces, seamless digital experiences, and agile operations. On the other hand, traditional banks are adapting to the digital landscape by embracing technological advancements, revamping their online and mobile banking platforms, and introducing innovative features.

Use Cases

Mobile banking is one of the prominent use cases in the fintech-driven banking sector. It allows users to perform various banking activities conveniently through mobile applications, including balance inquiries, fund transfers, bill payments, and more. Additionally, fintech has facilitated online account opening, simplifying the process and eliminating the need for in-person bank visits. Real-time payments, enabled by fintech solutions, ensure swift and secure transactions, enhancing customer experiences.

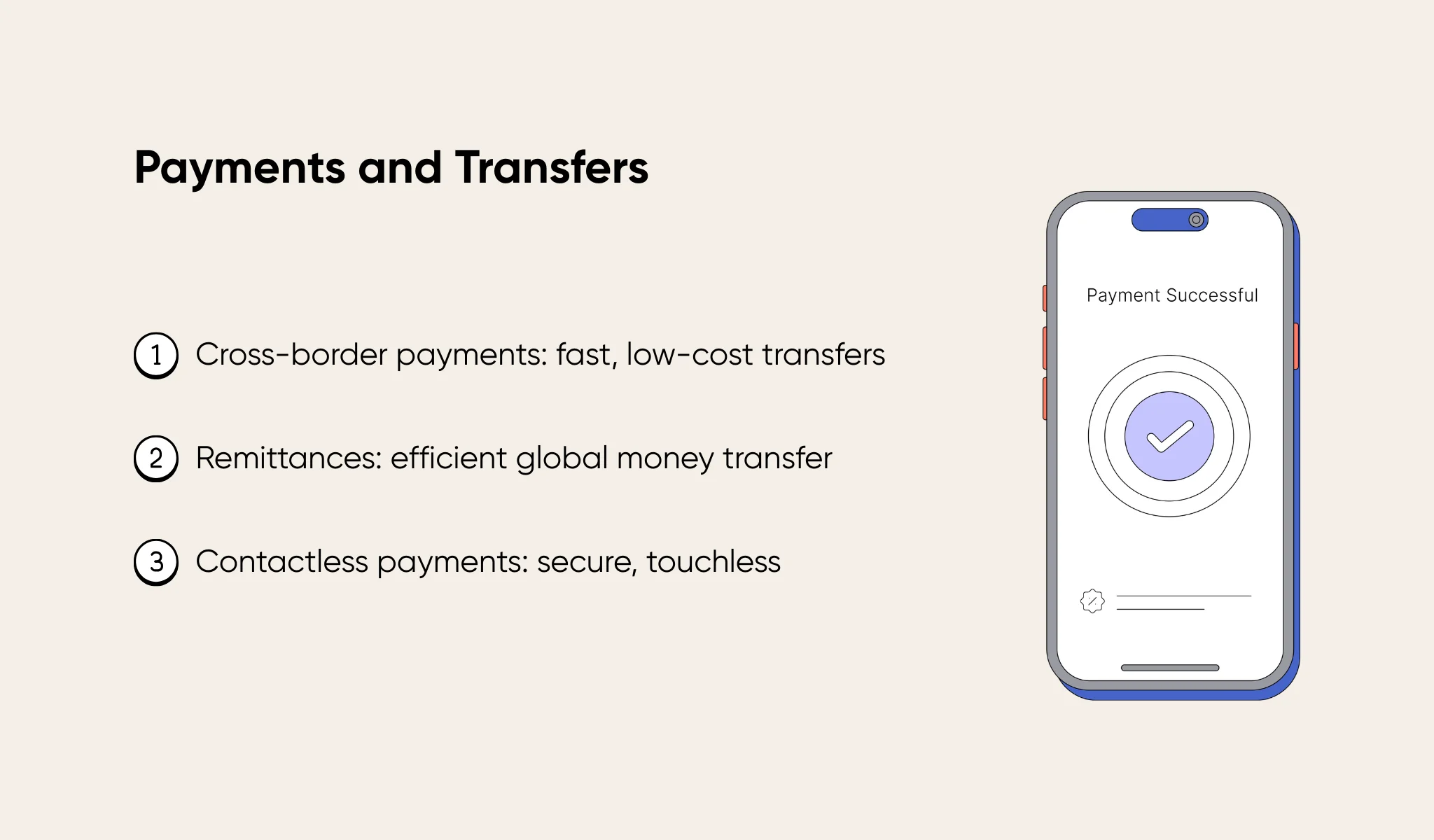

Payments and Transfers

The fintech revolution has dramatically impacted the payments and transfers landscape, introducing innovative solutions that simplify transactions and provide greater convenience. One such innovation is the ability to do money transfer online, which allows individuals to send money across borders quickly and securely without the need for traditional banking procedures.

Brief Overview

Peer-to-peer (P2P) payments are now a fully mature piece of fintech infrastructure. Digital wallets are a secure and convenient way to store payment credentials and conduct transactions seamlessly. Fintech also facilitated the rise of cryptocurrency and is now focusing on regulated stablecoins, tokenized assets, settlement layers, and institutional crypto custody.

Use Cases

Fintech has revolutionized cross-border payments, reducing complexities and transaction costs associated with international transfers. It enables individuals and businesses to send and receive money globally faster and more transparently. Remittances, a crucial aspect of global finance, have also been transformed by fintech, allowing efficient and cost-effective transfer of funds across borders. Furthermore, contactless payments have gained popularity, especially in recent years, providing a secure and touchless payment experience through various fintech-driven solutions.

Lending

Fintech has disrupted the lending landscape, offering alternative lending platforms and streamlined processes that cater to the evolving needs of borrowers.

Brief Overview

Peer-to-peer (P2P) lending platforms have revolutionized the lending industry by directly connecting borrowers with lenders through online platforms. These platforms leverage fintech to facilitate loan transactions, removing the traditional intermediaries and reducing costs. Digital lending, another fintech innovation, provides borrowers with simplified loan application processes, faster approvals, and customized lending options.

Use Cases

Fintech-driven lending has opened doors to payday loans, allowing borrowers to access funds quickly and conveniently through digital channels. Microcredit, often facilitated by fintech platforms, addresses the financial needs of individuals and small businesses by providing small loan especially SBA loans with minimal documentation requirements. Additionally, fintech has revolutionized credit scoring models, utilizing alternative data and advanced algorithms to assess creditworthiness beyond traditional credit metrics.

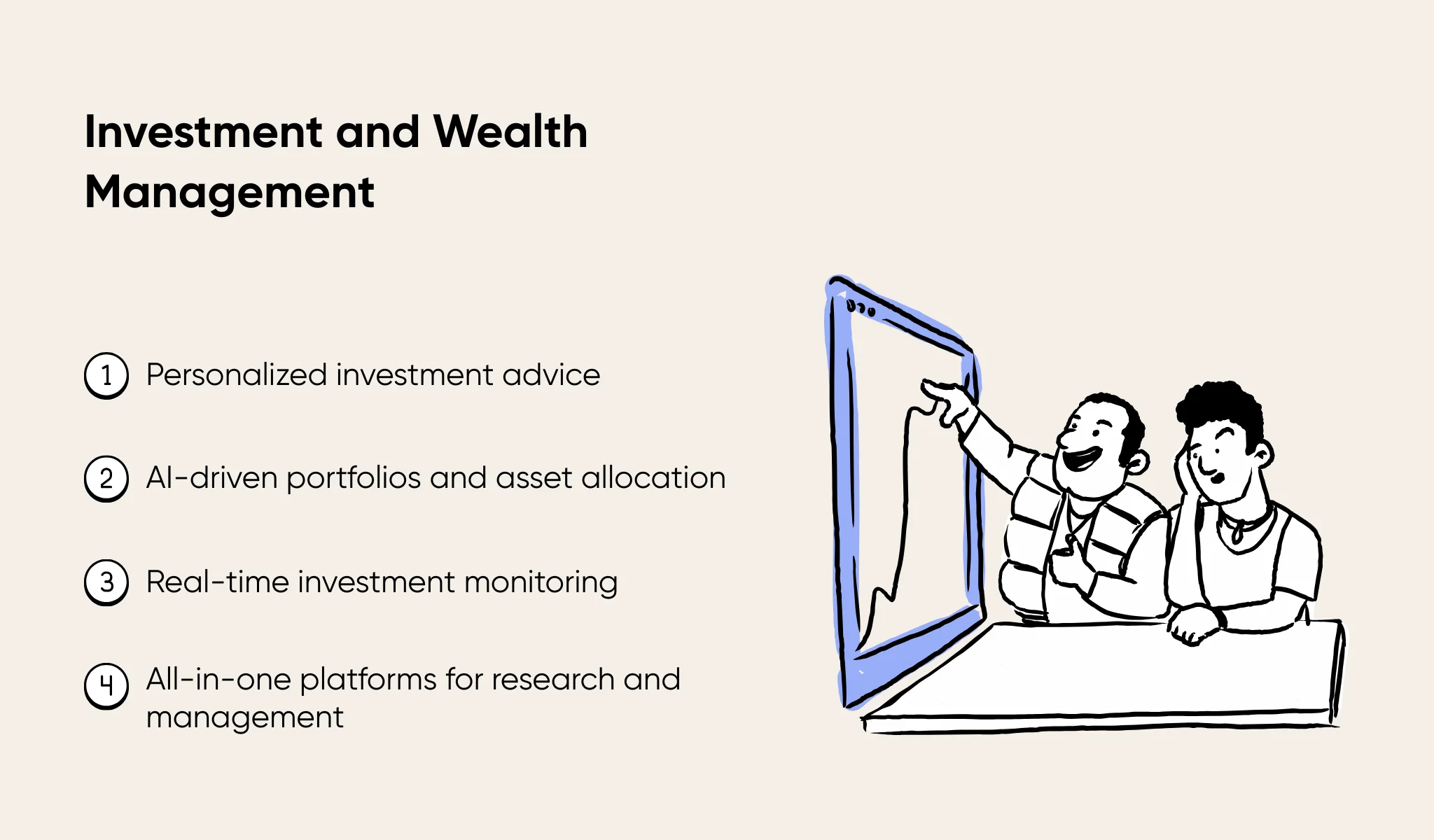

Investment and Wealth Management

Fintech has transformed investment and wealth management, democratizing access to financial markets and offering innovative tools for personalized financial planning.

Brief Overview

Robo-advisors, powered by fintech algorithms and machine learning, provide automated investment advice and portfolio management services. These platforms offer investors diversified investment options, personalized recommendations, and cost-effective solutions. Furthermore, online trading platforms have disrupted traditional brokerage services, enabling individuals to conveniently trade stocks, commodities, and other financial instruments through intuitive digital interfaces. Before choosing savings accounts, investment products, or financial tools, users can rely on a money comparison website to evaluate interest rates, fees, and market options with greater transparency.

Use Cases

Fintech-driven investment and wealth management solutions cater to individuals' financial goals and risk preferences, providing personalized investment advice. These solutions offer optimized portfolios, asset allocation strategies, and real-time monitoring by leveraging AI and data analytics. Platforms like an excellent all-in-one platform can further support investors by streamlining research and decision-making. Fintech innovations in this sector empower individuals to make informed investment decisions and manage their wealth efficiently.

Insurance (Insurtech)

Fintech has brought forth significant changes in the insurance industry, giving rise to "insurtech" and introducing innovative approaches to insurance services.

.webp)

Brief Overview

Digital brokers have emerged due to fintech advancements, allowing individuals to easily compare insurance policies, obtain quotes, and purchase coverage online. Insurtech also utilizes AI-based risk assessment models, leveraging data analytics to accurately assess risks, determine premiums, and streamline insurance underwriting processes.

Use Cases

Fintech-driven insurance solutions have led to usage-based insurance, where premiums are determined based on an individual's usage or behavior, such as mileage or driving habits. Personalized insurance policies have also gained traction, allowing individuals to tailor coverage to their specific needs and preferences.

By leveraging fintech in the insurance sector, customers can enjoy more accessible, flexible, and personalized insurance solutions, while insurers benefit from streamlined operations and improved risk assessment capabilities.

Regulatory Technology (RegTech)

Fintech's influence extends to regulatory technology (RegTech), transforming compliance and risk management practices within the financial industry.

.webp)

Brief Overview

RegTech offers innovative solutions that simplify and streamline compliance processes for financial institutions. It enables automated monitoring of regulatory requirements, real-time reporting, and robust risk management frameworks. These solutions leverage fintech innovations such as data analytics, AI, and machine learning to ensure regulatory compliance while reducing costs and improving efficiency.

Use Cases

RegTech solutions are critical in combating financial crimes such as money laundering. They employ advanced algorithms and data analysis to detect suspicious activities, verify customer identities, and ensure adherence to Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. Fintech-driven RegTech solutions enhance the effectiveness of compliance measures and contribute to a more secure financial ecosystem. As fintech companies scale across jurisdictions, regulatory obligations grow more complex. Beyond automated tools, organizations often rely on experienced financial attorneys to structure transactions, interpret evolving regulations, and manage legal risks in areas like banking relationships, structured finance, and fintech compliance.

Fintech has revolutionized various segments of the finance industry, from banking and payments to lending, investment and wealth management, insurance, and regulatory technology. By embracing fintech innovations, businesses and individuals can benefit from enhanced accessibility, efficiency, and personalized services across these sectors. Technology integration in finance continues to reshape the industry, offering transformative solutions and improving the financial landscape.

Role of Software in Fintech Innovation

Software is pivotal in driving fintech innovation, enabling the development and implementation of cutting-edge solutions that reshape the finance industry. Through sophisticated algorithms, data analytics, and automation, fintech software empowers businesses to enhance efficiency, improve customer experiences, and unlock new possibilities.

Automation and Efficiency

Fintech software streamlines processes, automating repetitive tasks such as transaction processing, data entry, and compliance checks. This reduces manual effort, minimizes errors, and enables faster, more accurate results. For example, software-based robo-advisors automate investment management, providing personalized advice and portfolio management at scale.

Advanced Analytics

Fintech software leverages data science and analytics to derive valuable insights from vast financial data. By analyzing market trends, customer behaviors, and risk factors, businesses can make data-driven decisions, identify investment opportunities, and tailor financial products and services to individual needs.

Enhanced Customer Experiences

Fintech software strongly emphasizes user-centric design and personalized experiences. Mobile applications and digital platforms enable convenient and intuitive access to financial services, allowing customers to manage their finances, make payments, and seek financial advice from the comfort of their devices. These platforms often include integrated tools for improved customer experience. For example, Clutch, a car marketplace, provides auto financing, and so they've integrated an auto loan calculator in Canada, providing users with instant calculations and comparisons that enhance their decision-making experience without leaving the app. Chatbots and AI-powered customer service solutions improve response times and provide instant support.

Integration and Collaboration

Fintech software facilitates seamless integration between financial institutions, startups, and other stakeholders. Open banking APIs enable secure data sharing, allowing customers to access their financial information across multiple platforms and enabling collaboration between service providers. This promotes innovation, enables partnerships, and expands the range of financial products and services available to customers.

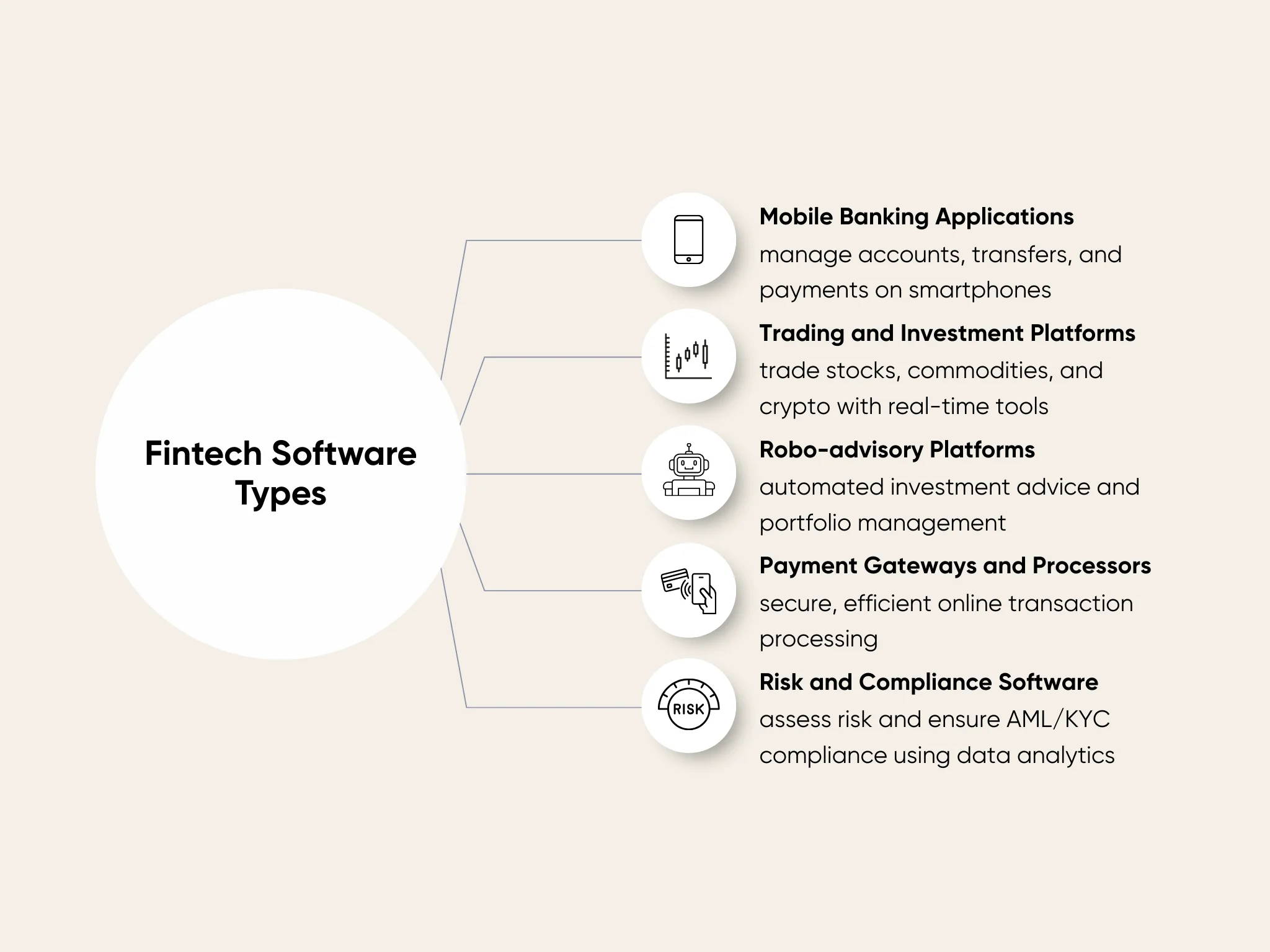

Fintech Software Types and Their Uses

Different fintech software serves various purposes in the finance industry:

- Mobile Banking Applications: Users can perform banking activities on their smartphones, such as transfers, payments, and account management.

- Trading and Investment Platforms: Power online platforms for trading stocks, commodities, and cryptocurrencies, offering real-time data and advanced tools.

- Robo-advisory Platforms: Utilize algorithms to provide automated investment advice and portfolio management based on investors' profiles and goals.

- Payment Gateways and Processors: Enable secure and efficient processing of financial transactions for online payments and e-commerce.

- Risk Management and Compliance Software: Aid in risk assessment and compliance with regulations like AML and KYC, using data analytics and machine learning algorithms.

Security and Regulatory Considerations in Fintech Software Development

Developing secure and compliant fintech software safeguards customer data and ensures regulatory adherence. Fintech firms must address the following considerations:

Cybersecurity Measures

Fintech software must implement robust security protocols, including encryption, two-factor authentication, and secure data storage, to protect sensitive financial information from unauthorized access and cyber threats.

Compliance with Regulations

Fintech software development should adhere to relevant financial regulations and standards, such as those set by regulatory bodies like the Securities and Exchange Commission (SEC) and the Financial Conduct Authority (FCA). Compliance solutions and practices must be integrated into the software to ensure adherence to regulatory requirements.

Data Privacy and Protection

Fintech software must comply with data protection laws like Europe's General Data Protection Regulation (GDPR). It should incorporate measures to handle and store personal and financial data securely while providing transparency and control to users over their data.

Regular Audits and Assessments

Fintech software should undergo regular security audits and assessments to identify vulnerabilities, address potential risks, and ensure compliance with ongoing security and regulatory standards.

Scalability and Reliability

Fintech software should be designed to handle increasing transaction volumes and user demands. It should be reliable, provide uninterrupted service, and have robust disaster recovery plans.

By considering these security and regulatory aspects during fintech software development, businesses can build trust with customers, mitigate risks, and ensure the integrity and reliability of their financial technology solutions.

Cybersecurity Challenges in Fintech

Cybersecurity is a critical concern for fintech companies in the digital age due to the sensitive nature of financial transactions and data. Fintech faces unique cybersecurity challenges that must be addressed to safeguard customer information and maintain the integrity of financial systems. Here are the critical challenges faced by fintech in cybersecurity:

Data Breaches and Unauthorized Access

Fintech companies handle vast amounts of sensitive financial data, making them attractive targets for cybercriminals. Data breaches can result in financial loss, identity theft, and company reputation damage. To help mitigate these risks, organizations can utilize a digital footprint checker to identify exposed data, monitor potential vulnerabilities, and proactively secure their online presence.

Regulatory Compliance

Fintech companies must adhere to stringent data protection and privacy regulations. Failure to comply can lead to significant fines, legal consequences, and reputational damage.

Emerging Threats

As technology evolves, so do cybersecurity threats. Fintech companies must stay vigilant against emerging threats such as ransomware, phishing attacks, malware, and social engineering.

Third-party Vulnerabilities

Fintech companies often rely on third-party service providers, increasing the risk of cybersecurity vulnerabilities. Ensuring the security of these partnerships and managing third-party risk is crucial.

User Authentication and Identity Verification

Fintech companies must implement robust authentication and verification methods to prevent unauthorized access and identity fraud.

Security in Mobile Applications

With the rise of mobile technology, securing fintech applications becomes crucial. Protecting data and transactions on mobile devices and addressing vulnerabilities specific to mobile platforms is a significant challenge.

Addressing these challenges requires proactive measures, including implementing robust security protocols, conducting regular vulnerability assessments, investing in cybersecurity infrastructure, and educating employees and customers on cybersecurity best practices. By prioritizing cybersecurity, fintech companies can protect their systems, gain customer trust, and contribute to a more secure financial ecosystem.

Key Takeaways

Software development is right in the middle of every industry’s push for innovation. Nowhere is that more true than in the fintech industry. From everyday conveniences like real-time transactions to advanced tech that supports the global financial network, finance and software are now inseparable.

As a financial company, remember that tapping into the potential of fintech involves building up scalable architectures, investing in advanced data analytics, and identifying opportunities for automation. All of these make it easier to operate securely at scale, maintain constant compliance, and deliver better and faster financial services.

Looking to build a fintech solution designed around your specific business realities? Aloa can help. With our extensive AI software dev expertise, we can prototype, develop, and support custom fintech software across a wide range of budgets and technical demands. Talk to us about your ideas today!

If you’d like to explore some more, you can talk to like-minded individuals on our Discord server or read up on other tech industry insights on our blog. Alternatively, check out our newsletter: Byte-Sized, where I collect all of the latest developments on new models, tools, and AI in general from the past 24 hours.

FAQs

How does fintech improve financial accessibility for individuals and businesses?

Fintech makes financial services more accessible by lowering costs, removing geographic barriers, and creating digital products like mobile banking, instant payments, and alternative lending.

What role do fintech startups play in challenging traditional financial institutions?

Fintech startups compete with larger institutions by focusing on areas that they struggle to modernize quickly. These include:

- Speed: Fintech startups have shorter development cycles and are often cloud-native, allowing them to roll out features and products at a faster rate and respond to market changes more easily.

- User experience: Startups have the advantage of working with a clean slate, allowing them to bake in superior UX, unlike traditional institutions that have to struggle with legacy systems.

- Niche problems and use cases: Bigger banks try to serve everyone, but fintech startups have more success by solving narrow problems exceptionally well, such as cross-border payments for specific regions or cash-flow lending for small businesses.

How do fintech solutions ensure the security of financial transactions?

Fintech platforms rely on encryption, tokenization, multi-factor authentication, and continuous fraud monitoring to secure transactions. Many also align with global compliance standards and build security into their architecture from day one.

In what ways is blockchain technology utilized in fintech?

Blockchain has dozens of uses in fintech. The most common ones include:

- Cross-border payments: Since they don’t depend on large banking networks, cryptocurrencies powered by blockchain can be transferred across borders faster and at lower cost.

- Smart contracts: These are self-executing programs stored on a blockchain that automatically enforce financial agreements when conditions are met. They can be used for automated settlement, escrow, and programmable payments.

- Transparent transaction records: Cryptocurrency transactions are so trusted because they use distributed ledger technology, which spreads out transaction data so no one entity has control of it. Most of this tech is powered by blockchain.

How is fintech impacting personal finance management for individuals?

Fintech tools now offer real-time spending insights, automated savings, and AI-driven budgeting that adapts to user behavior. Apps like Revolut and Chime help users track spending as it happens, automate savings and bill management, receive instant alerts, and make day-to-day financial decisions with greater visibility and control.

What are the major challenges facing the fintech industry today?

Key challenges include:

- Regulatory complexity: Global data protection laws constantly evolve. They can also become fragmented across jurisdictions, confusing compliance.

- Rising customer acquisition costs: Acquiring new customers is a lot more expensive nowadays, so there’s more pressure for fintech to account for retention, lifetime value, and embedded distribution to justify that cost.

- Maintaining security as platforms scale: With larger transaction volumes and deeper integration, fintech platforms face increased exposure to fraud, identity abuse, API attacks, and third-party risk.

- Legacy system integration: Outdated banking infrastructure and third-party providers can slow down development and limit flexibility.

The custom software we build at Aloa solves all of these by design. We take a 360-degree look at your security, compliance, and scalability needs to make sure every feature works together to mitigate these challenges.

Which companies compete in the financial technology services market?

Competition in fintech services includes payment processors, digital banks, and enterprise finance platforms such as Adyen, Fiserv, and Plaid. These companies differentiate through scale, integrations, and specialization. Aloa stands out by focusing on designing custom-built fintech products rather than selling a single software platform.