In 2024, the financial landscape is witnessing a profound shift as Fintech vs Banks becomes the central theme of the industry’s competitive dynamics. FinTech startups, known for their innovative technology-driven solutions, are challenging the dominance of traditional banks, which have long held sway in the industry.

However, amidst this rivalry, both sides are compelled to adapt and innovate, benefiting consumers with a broader range of financial services and options.

Aloa, a software outsourcing firm, boasts industry experience and actively keeps pace with emerging trends to meet clients’ needs effectively. Aloa’s dedication to staying up-to-date with innovative technologies ensures they deliver high-quality solutions aligned with the latest advancements in the field.

In this blog, we’ll unravel the Fintech vs Banks, shedding light on the contrasting approaches to financial services and their impact on consumers. By the end, you’ll have a clearer understanding of the evolving dynamics between innovative Fintech disruptors and the established banking sector.

Let’s dive in!

FinTech vs Banks: What’s the Difference?

The primary distinction in comparing FinTech vs Banks lies in their approach to financial services. FinTech companies offer convenient and user-friendly solutions aimed at modernizing banking experiences. On the other hand, traditional banks prioritize stability and trust in their service delivery.

FinTech vs banks extends beyond technology to encompass the overall customer experience and the level of adaptability to evolving market trends. This ongoing competition spurs innovation, benefiting consumers with diverse financial options tailored to their preferences. Understanding these differences is essential for individuals seeking to navigate the complex landscape of modern finance effectively.

What is FinTech?

FinTech, short for Financial Technology, encompasses various innovative technologies and business models that aim to improve and automate financial services, including the use of technology such as mobile payments, blockchain technology, and artificial intelligence. The FinTech industry leverages advancements in machine learning to enhance efficiency and accessibility in the financial services industry.

Here are the most common types of FinTech:

- Payment Processing: Facilitates electronic transactions and payments through platforms like mobile payment apps and digital wallets. An example is PayPal, which offers a popular electronic payment and transaction platform.

- Peer-to-Peer (P2P) Lending: Connects borrowers directly with investors for loans, bypassing traditional financial institutions. LendingClub is an example of this, connecting borrowers with investors looking to fund personal loans.

- Robo-Advisors: Utilizes algorithms to provide automated investment advice and portfolio management services. Betterment, which provides automated investment advice and portfolio management services, is an example.

- Blockchain and Cryptocurrency: Utilizes blockchain technology for secure and transparent transactions, digital asset management, and decentralized finance applications. An example is Bitcoin, a well-known digital currency operating on blockchain technology.

- Personal Finance Management (PFM): Offers digital tools for individuals to manage their finances, including budgeting, expense tracking, and financial planning features. Mint is an example of this, offering a comprehensive budgeting, expense tracking, and financial planning platform.

These types represent just a subset of the diverse range of services and solutions offered within the FinTech market, providing insight into the dynamic industry overview of FinTech and its evolving landscape within the financial industry.

What is Traditional Banking?

Traditional banking, within the world banking system, encompasses a wide array of financial services provided by brick-and-mortar banks with physical branches, including deposit accounts, loans, mortgages, wealth management, and bank account services.

They are often facilitated through traditional channels like telephone and mail. Additionally, traditional banking involves the issuance and management of credit cards and debit cards. Central banks maintain regulatory oversight to ensure stability and integrity within the financial system.

Traditional banks, including corporate banks, operate under regulatory frameworks and are recognized for their stability, reliability, and long-standing presence in the financial system and banking industry. They often prioritize face-to-face interactions and personalized services, building customer trust over time and contributing to the overall stability of the banking system.

Here are the most common types of banks:

- Retail Banks: These banks cater to individual consumers by offering various financial services, including savings and checking accounts, loans, and mortgages, making them accessible to the general public for everyday banking needs.

- Commercial Banks: Geared towards businesses, commercial banks provide specialized financial services such as business loans, corporate banking, and treasury management, aiding enterprises in managing their financial operations and facilitating growth.

- Investment Banks: Focused on corporate and institutional clients, investment banks specialize in providing financial advisory services, underwriting, facilitating mergers and acquisitions, and supporting businesses in strategic financial decisions and transactions.

- Private Banks: Catering to high-net-worth individuals and families, private banks offer personalized financial services and wealth management solutions, ensuring tailored financial strategies and exclusive services to meet the unique needs of affluent clients.

These diverse types of banks cater to various customer needs within the financial sector, offering specialized services to individual consumers and businesses, ensuring a comprehensive range of banking options for customers worldwide.

Core Differences Between FinTech and Banks

Understanding FinTech vs banks is essential for navigating the diverse financial services available. Here are the core differences between FinTech and banks, highlighting the distinct approaches and strategies each sector employs to meet the needs of consumers and businesses alike:

- Speed and Agility: FinTech companies excel in agility and speed, leveraging innovative technology to provide quick and efficient financial services, while traditional banks, due to their larger size and established infrastructure, may face challenges in adapting to rapidly changing market demands, illustrating the ongoing competition of fintech vs banks.

- Innovation and Adaptability: FinTech firms prioritize innovation and adaptability, constantly introducing new technologies and solutions to enhance customer experiences, whereas banks often rely on legacy systems and may encounter hurdles in implementing innovative solutions due to regulatory constraints and organizational structure.

- Customer-Centric Approach: When it comes to the customer-centric approach of FinTech vs banks, FinTech companies adopt a customer-centric approach, offering personalized and user-friendly financial solutions tailored to individual needs, while banks may struggle to provide the same level of customization, potentially being perceived as more impersonal due to standardized offerings and processes.

- Cost Efficiency: FinTech firms operate with lower overhead costs compared to traditional banks, leveraging digital platforms for service delivery, which may result in potentially lower fees and expenses for customers, while banks may incur higher operational costs associated with maintaining physical branches and legacy systems, potentially leading to higher fees for customers.

- Regulatory Compliance: FinTech companies navigate complex regulatory landscapes to ensure compliance with financial regulations, which can sometimes be challenging for newer entrants, while traditional banks typically have established compliance procedures to manage regulatory requirements effectively, although they may encounter difficulties adapting to evolving regulatory frameworks.

Grasping the fundamental disparities of FinTech vs banks illuminates the evolving dynamics within the financial sector, shaping the choices available to consumers and businesses. By recognizing the core differences between FinTech and banks, individuals and organizations can make informed decisions that align with their specific financial goals and preferences.

Use Case For FinTech Solutions

Here’s how FinTech solutions, with their innovative fintech features, diverge from traditional banking practices in fintech vs banks, emphasizing the increasing demand to hire FinTech software developers for cutting-edge solutions.

Digital Payments

FinTech solutions are pivotal in driving digital transformation within the fintech ecosystem by offering convenient and secure digital payment options such as mobile wallets, peer-to-peer (P2P) money transfer solutions, and contactless payments. They address the growing demand for cashless transactions in personal and business settings, streamlining the payment process and providing users with a seamless and efficient transaction experience.

With the rise of e-commerce and digital commerce trends, FinTech digital payment solutions developed by leading fintech developer companies have become indispensable for individuals and businesses seeking fast, reliable, and secure payment methods.

Online Lending

FinTech businesses and platforms facilitate online lending, providing individuals and small businesses with quick and accessible financing options, including specialized funding programs for startups. These programs often offer streamlined application processes and competitive interest rates, designed to support the unique needs of emerging companies.

By leveraging technology and data-driven algorithms, these platforms enhance financial inclusion, fostering economic growth and entrepreneurship in the FinTech sector. FinTech online lending platforms empower borrowers seeking hassle-free access to capital, transforming the lending landscape and catering to the evolving needs of borrowers.

Robo-Advisory Services

FinTech companies introduce robo-advisory services that utilize algorithms and automation to offer personalized investment advice and portfolio management solutions. These services empower individuals to make informed investment decisions based on their financial goals and risk tolerance.

By democratizing access to investment advice and portfolio management tools, FinTech robo-advisory services cater to a broader audience. They enable novice investors and individuals with limited investable assets to participate in the financial markets, fostering wealth creation and financial empowerment.

Blockchain and Cryptocurrency

As fintech vs banks intensifies, FinTech banking continues to leverage blockchain technology to provide alternative financial services and investment opportunities, including digital security and currency exchange, thereby disrupting traditional banking systems.

With the emergence of cryptocurrencies like Bitcoin and Ethereum, FinTech blockchain solutions enable individuals and businesses to access decentralized financial products and services. They revolutionize how assets are stored, transferred, and managed, fostering innovation and disruption in the financial industry.

Personal Finance Management (PFM)

When comparing the benefits of fintech vs banks, it’s evident that FinTech platforms offer individuals greater control over their financial well-being through personal finance management tools and applications.

With the rise of digital banking and financial wellness trends, FinTech PFM solutions are crucial in promoting financial literacy and empowering users to achieve their financial objectives. They facilitate informed financial decision-making and long-term planning, helping users save for retirement, pay off debt, or build an emergency fund.

Use Cases For Traditional Banking Solutions

Traditional banking solutions have long been the cornerstone of the financial industry. However, in the landscape of fintech vs banks, these solutions are now facing increasing pressure to innovate and adapt to the changing needs of consumers. Here are the use cases for traditional banking solutions:

Retail Banking Services

Traditional banks offer various retail banking services tailored to consumers, including savings accounts, checking accounts, loans, and mortgages. These services provide customers with essential financial tools for managing their day-to-day finances, saving for the future, and financing significant purchases such as homes and vehicles.

Business Banking Services

When it comes to FinTech vs banks, traditional banks provide comprehensive business banking services to support the financial needs of businesses, iincluding business loans, corporate banking, and a treasury management system. These services help businesses manage their cash flow, access capital for growth and expansion, and navigate complex financial transactions to support their operations and strategic objectives.

Wealth Management

In wealth management of Fintech vs banks, traditional banks offer wealth management services to high-net-worth individuals and families, including investment advisory services, portfolio management, and estate planning. These services help clients grow and preserve their wealth over time, providing personalized financial strategies and guidance to achieve their goals and secure their future. For individuals seeking more specialized, long-term guidance beyond standard banking products, working with a private wealth advisory firm can offer tailored investment strategies, estate planning support, and personalized portfolio oversight.

Investment Banking

Traditional banks specialize in providing investment banking services to corporations, institutional investors, and governments, including financial advisory services, underwriting, and facilitating mergers and acquisitions, providing purchase price allocation services. These services support corporate finance activities and strategic transactions, helping businesses raise capital, restructure their operations, and pursue growth opportunities in the global marketplace.

Mortgage Services

Traditional banks offer mortgage services to individuals and families, including mortgage loans, refinancing, and home equity lines of credit. These services enable customers to finance home purchases, refinance existing mortgages to lower interest rates, or access home equity for major expenses, providing essential financial support for homeownership and real estate investment.

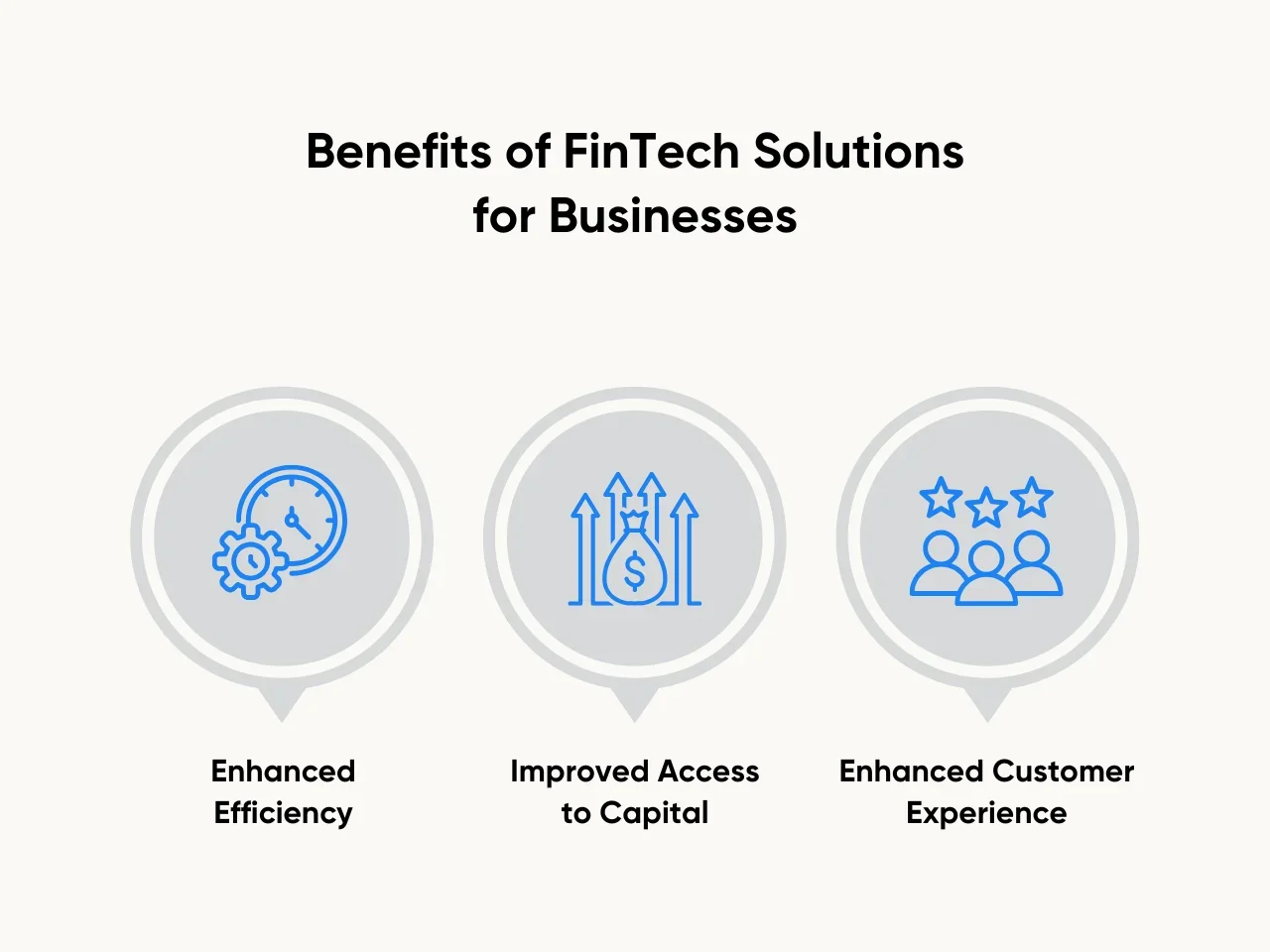

Benefits of FinTech Solutions for Businesses

FinTech solutions, developed by fintech app developers, offer businesses innovative financial tools and services tailored to meet the demands of the modern marketplace. Here are the benefits of FinTech solutions for businesses seeking innovative financial solutions:

Enhanced Efficiency

FinTech solutions streamline business operations by automating repetitive tasks, reducing manual errors, and improving efficiency. For example, digital payment platforms allow businesses to process transactions quickly, saving time and resources compared to traditional payment methods.

Improved Access to Capital

FinTech platforms offer alternative lending options, such as peer-to-peer lending and online lending, providing businesses with easier access to capital than traditional banks. This enables small and medium-sized enterprises (SMEs) to secure funding for growth and expansion without the extensive paperwork and stringent requirements often associated with traditional loans. Businesses can also explore options like a high-limit business credit card to manage cash flow, finance large purchases, and gain additional financial flexibility alongside traditional or FinTech lending solutions.

Enhanced Customer Experience

FinTech solutions prioritize customer-centric approaches, offering personalized and user-friendly experiences that cater to the needs and preferences of modern consumers. For instance, mobile banking apps provide convenient access to financial services anytime, anywhere, enhancing customer satisfaction and loyalty.

Benefits of Traditional Banking Solutions for Businesses

In the benefits of FinTech vs banks, traditional banking solutions have long been the backbone of financial services, offering stability and a wide range of offerings to businesses of all sizes. Here are the benefits of traditional banking solutions for businesses.

Comprehensive Financial Services

Traditional banking solutions offer a wide range of comprehensive financial services tailored to meet the diverse needs of businesses. These services include business loans, corporate banking, treasury management, trade finance, and cash management solutions, providing businesses with essential tools to manage their finances effectively and support their growth and expansion.

Relationship-Based Approach

The emergence of FinTech solutions has revolutionized traditional banking practices, offering innovative and streamlined financial services tailored to the needs of today’s consumers and businesses in the ongoing competition of fintech vs banks. This personalized approach fosters long-term relationships between banks and businesses, allowing customized solutions and tailored financial strategies that align with each business’s specific needs and objectives.

Trust and Stability

Traditional banks are known for their trustworthiness and stability, offering security and reliability to business owners who rely on their financial services. This trust and stability are essential for businesses, especially during economic uncertainty or market volatility, as traditional banks provide a stable foundation for businesses to navigate challenging financial situations and ensure their financial well-being.

Key Takeaway

The ongoing competition of FinTech vs banks is reshaping the financial landscape, providing consumers and businesses with a diverse range of options for their financial needs. While traditional banks offer stability and trust built on years of industry experience, FinTech brings innovation, agility, and convenience, offering customers cutting-edge solutions tailored to their modern lifestyles.

As FinTech continues to push boundaries and challenge traditional banking norms, it’s evident that its forward-thinking approach is driving the evolution of the financial industry towards a more customer-centric and technologically advanced future.

Start developing your fintech solution by exploring Aloa’s developer hiring page. We’ll link you with the ideal team who can turn your idea into a successful reality in today’s highly competitive market!