Bank fraud has gotten ugly. In 2023 alone, banks lost more than $10 billion to confirmed fraud, and attempts shot up by 149%. Fraudsters are faking identities, cloning voices with AI, and even hijacking IoT-connected devices. Every new attack feels one step ahead of the old defenses.

You probably feel that squeeze daily. Legacy rule-based tools throw off alerts but miss the fraud that matters. Regulators want airtight compliance. Leadership pushes for proof of ROI. And all the while, customers expect every payment to clear instantly without a hitch. It’s pressure from every angle, with little room for mistakes.

Instead of forcing one-size-fits-all tools into place, many banks are turning to partners who can tailor fraud detection to their systems. At Aloa, we design custom AI fraud detection systems that slot into the banking platforms you already run. Our finance AI development services help banks scale detection, cut false positives, and roll out upgrades without derailing daily operations. We’ve seen how shaving weeks off implementation or reducing alert fatigue can completely change outcomes for teams like yours.

This guide is your shortcut. We’ll cover seven systems for real-time fraud detection in the banking sector: how they work, what it takes to integrate them, what kind of ROI you can expect, and how they hold up to compliance. By the end, you’ll have a clear picture of what’s worth your time and budget.

Understanding Modern Banking Fraud Landscape

Real-time fraud detection in the banking sector means scanning every transaction in milliseconds with AI and machine learning to catch suspicious behavior before it slips through. It allows banks to block identity theft, card fraud, and money laundering attempts as they happen.

The old approach was rigid rule checks. Today, AI-based fraud detection in banking works more like intuition backed by massive datasets. It learns from millions of behaviors (how people swipe, where they log in, what devices they use) and calls out anything that doesn’t fit. That shift matters because criminals aren’t standing still.

Some of the biggest financial crimes banks are battling today include:

- Synthetic Identity Fraud: A criminal mixes stolen details with fake ones to build an entirely new “person.” That fake person opens accounts, applies for loans, and racks up debt that banks rarely recover.

- Deepfake Authentication Bypass: Think cloned voices or faces tricking voice or facial recognition systems into letting fraudsters in.

- IoT Exploitation: ATMs, card terminals, and even smart devices at branches can be hijacked as attack points.

- Quantum Risks: Still emerging, but if quantum computing cracks encryption one day, unprepared banks will feel it first.

And it doesn’t hit every bank the same way. Smaller institutions often deal with phishing and account takeovers. Larger ones juggle massive financial transaction volumes across borders, where every region has its own compliance playbook. Put it together, and the bill is steep: around $600 billion a year in global cybercrime losses.

This is the new normal: adaptive fraud that requires adaptive defenses.

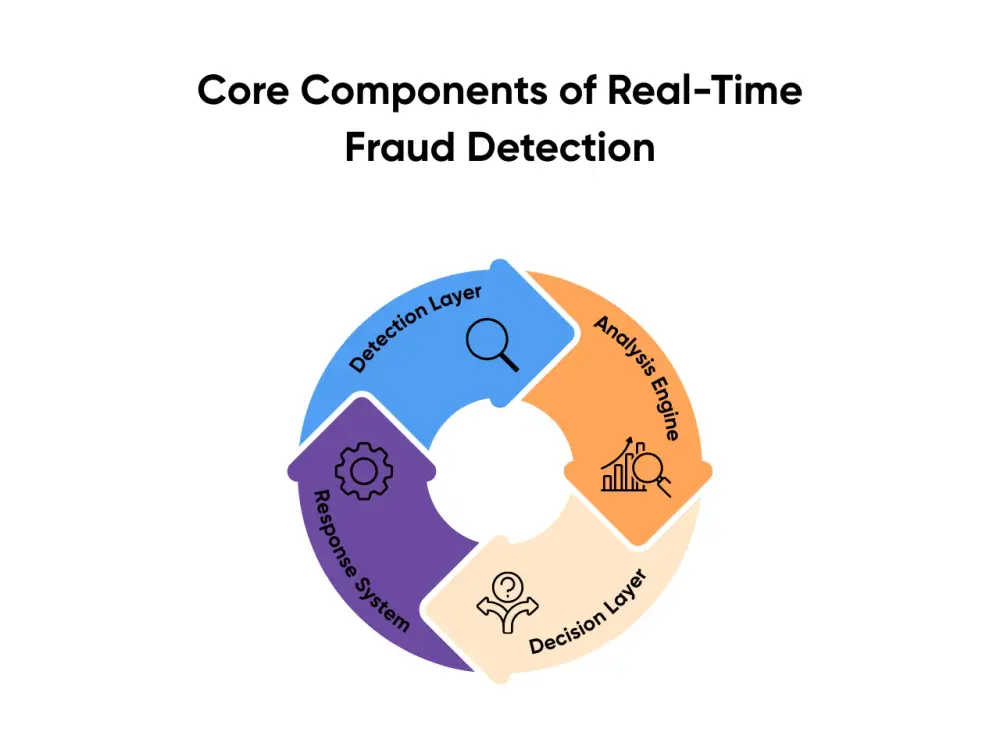

Core Components of Real-Time Fraud Detection

Picture your body’s immune system. It’s always scanning, looking for anything unusual, and neutralizing threats before you get sick. Real-time fraud detection is a similar concept but on steroids. It scans thousands of banking transactions every second without slowing down your customers.

And every strong setup runs on four moving parts:

- Detection Layer: Watches every transaction stream and pulls in details like device type, geolocation, spending patterns, and behavioral signals.

- Analysis Engine: Uses machine learning to compare those data points against past activity, spotting when something doesn’t line up.

- Decision Layer: Assigns a risk score on the spot, then decides whether to approve, pause, or block a legitimate transaction or a risky one.

- Response System: Acts in real time, like alerting analysts, blocking payments, or generating a compliance-ready report.

For these layers to work at scale, performance benchmarks matter:

- Speed: Modern platforms like AWS can run 200+ predictions per second, with responses under 100ms.

- Accuracy: Banks aim for detection rates over 95%, with false positives under 2% to keep customers happy.

- Scalability: Cloud-native, serverless setups flex automatically when transaction volumes spike.

Together, these pieces form the backbone of modern fraud defenses. Next up: the seven systems that banks are betting on to put these components into play.

7 Proven Fraud Detection Systems

Banks aren’t short on fraud detection tools, but the ones that matter will work under pressure. Each of the following fraud detection systems addresses a different part of the problem. The right mix depends on whether your institution is battling synthetic IDs, phishing scams, card fraud, or online payment risks.

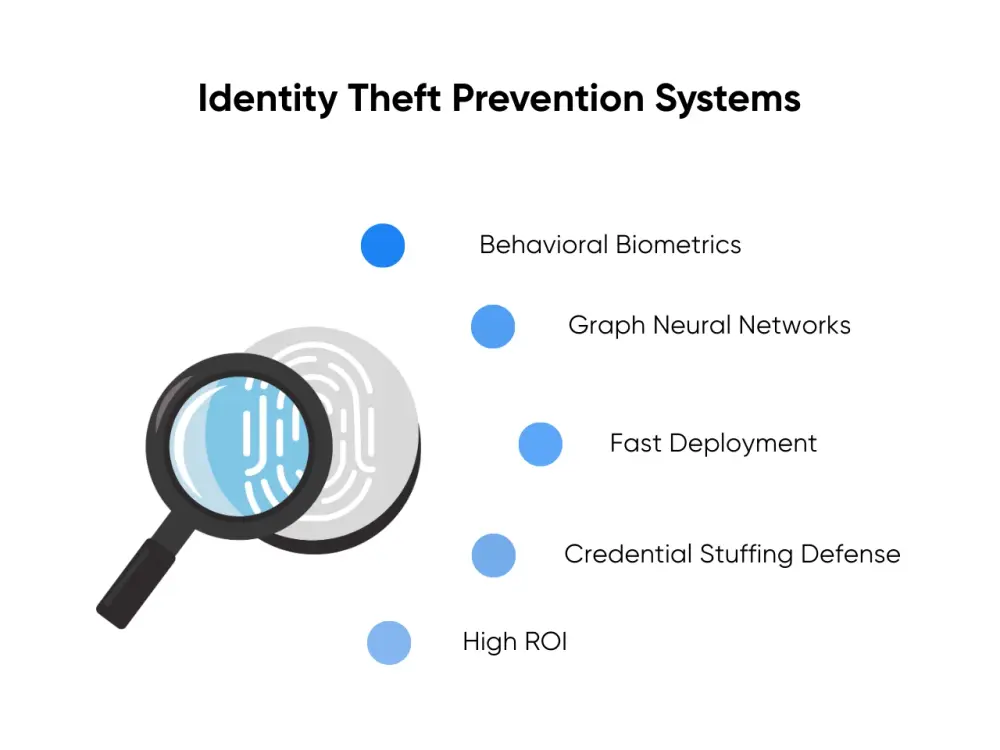

1. Identity Theft Prevention Systems

Identity theft drains millions every year, and synthetic identities only make it worse. Prevention systems here lean on subtle behaviors rather than surface-level credentials. Instead of relying only on passwords or two-factor codes, they add layers that fraudsters can’t easily fake:

- Behavioral biometrics track how people type, swipe, or move a mouse. These “digital fingerprints” are nearly impossible to fake and offer stronger signals than passwords.

- Graph neural networks reveal synthetic identities by finding hidden overlaps in data, like reused phone numbers or devices.

- Deployment speed is fast; pre-trained models often integrate in 2–4 weeks.

- Credential stuffing defenses shut down automated login attempts in real time.

- ROI averages $200K annually, thanks to fewer takeovers and unpaid synthetic loans.

Banks offering lots of consumer credit products tend to prioritize these systems since every fake account that gets through compounds long-term exposure.

2. Phishing Attack Prevention Systems

Phishing is no longer just suspicious emails. It now includes texts, fake login sites, and even deepfake phone calls. These systems allow banks to screen communications in real time and block scams before customers hand over access. They typically focus on a few capabilities:

- Natural language processing (NLP) scans email, SMS, and in-app messages for risky links, odd phrasing, or unusual patterns.

- Voice recognition helps call centers spot deepfake audio designed to mimic real customers.

- Implementation is quick, usually 3–6 weeks across all channels.

- Conversation monitoring flags when fraudsters are coaching victims through live transfers.

- Savings average $150K per year, largely from prevented wire fraud.

Community and regional banks often lean here because they’re prime targets for social engineering campaigns that play on customer familiarity and trust.

3. Credit Card Theft Prevention Systems

Card fraud remains the single most common attack vector, and customers expect their bank to catch it instantly. Prevention systems here are built to recognize what “normal” spending looks like and call out the rest. What banks gain usually looks like this:

- Predictive analytics models create profiles of customer behavior across time, merchant types, and transaction amounts.

- Cross-border analysis identifies fraud when cards suddenly show up in unusual countries or currencies.

- Deployments take 4–8 weeks, with pre-trained models easing the rollout.

- Instant deviation alerts flag high-value or out-of-pattern transactions before they settle.

- Typical ROI is $300K+ annually, cutting chargeback losses and fraud reimbursements.

Card-issuing banks get the most impact here because even small percentage drops in card fraud translate into significant bottom-line savings.

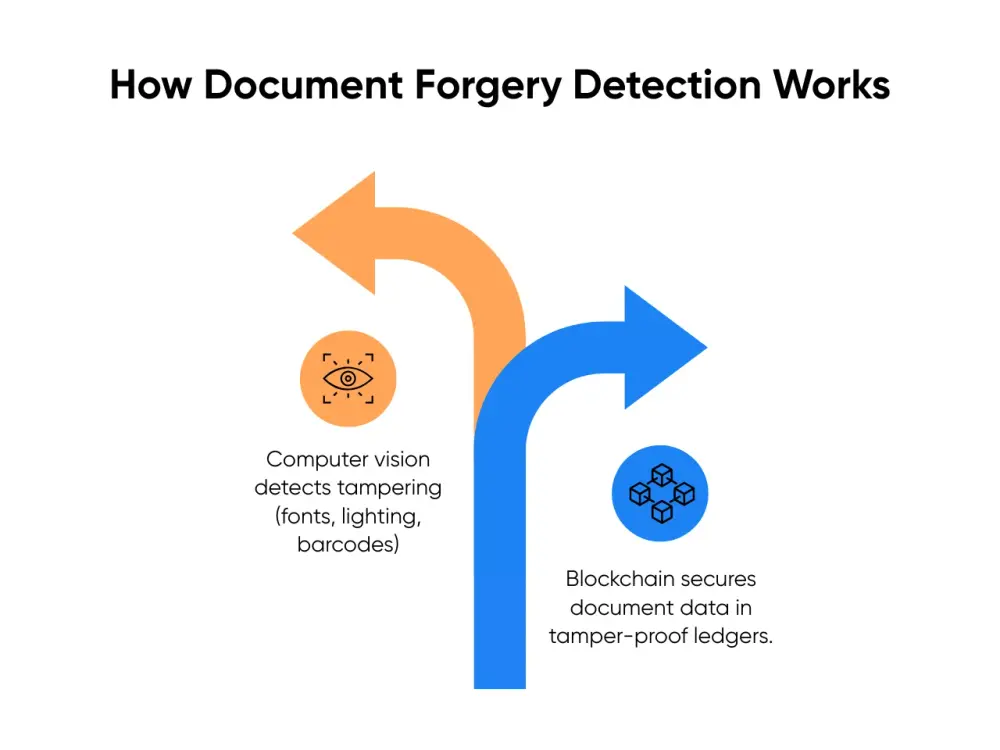

4. Document Forgery Detection Systems

Account fraud often begins at onboarding. If fake IDs or forged documents slip through, fraudsters gain access to credit and accounts that are nearly impossible to claw back. That’s why many banks add systems that double-check document authenticity:

- Computer vision inspects IDs and documents for tampering, like mismatched fonts, inconsistent lighting, or altered barcodes.

- Blockchain-backed records lock document data in tamper-proof ledgers for added assurance.

- Rollouts run 6–10 weeks, with API-ready tools speeding smaller bank adoption.

- Face-matching tools spot manipulated ID images or swapped photos.

- Annual savings average $250K, by stopping fraudulent accounts before they start.

Onboarding is where fraud attempts concentrate. That's why financial institutions with heavy online customer acquisition lean hard here.

5. Crypto Tracing Systems

More banks are touching crypto, whether directly or through customer transactions, and regulators are watching closely. Tracing systems give visibility into where funds are moving and whether they’re linked to known laundering networks. These tools typically deliver:

- Blockchain analytics that map flows between wallets, exchanges, and mixers.

- Multi-chain tracking that now covers privacy-focused coins once considered untraceable.

- Integration takes 8–12 weeks, with most banks starting by monitoring high-risk corridors.

- Rapid transfer detection catches split-and-hop laundering before funds scatter across wallets.

- ROI averages $400K annually, reducing exposure to regulatory fines and illicit transfers.

Financial services and other various industries experimenting with digital assets usually prioritize this system to reassure regulators and safeguard new revenue streams.

6. Verification Chatbot Systems

Fraud doesn’t always depend on tech. It often relies on manipulating people. Verification chatbots step in to protect customers during those moments when they’re most vulnerable:

- Analyzing conversations for scammer patterns, like hesitation or scripted answers.

- Voice biometrics that authenticate callers mid-conversation.

- Implementation takes 4–6 weeks, with cloud deployments making it smoother.

- Real-time alerts when customers are being coached by fraudsters.

- Financial impact averages $180K annually, largely by stopping authorized push payment scams.

Banks with high call center volumes or heavy retail exposure tend to see the most benefit here, improving both security and customer experience.

7. E-commerce Fraud Detection Systems

With online transactions and digital wallets exploding, e-commerce fraud is one of the fastest-growing threats. These systems give banks visibility into risky devices and patterns across online platforms. They usually bring:

- Device fingerprinting that ties accounts and sessions back to specific hardware.

- Linkage analysis that exposes coordinated fraud rings working across multiple accounts.

- Deployment takes 6–8 weeks, with models layered onto existing payment platforms.

- IoT transaction monitoring that covers smart devices tied into payment networks.

- Savings reach $350K annually, reducing fraudulent chargebacks for banks processing large online volumes.

Banks supporting retailers or payment processors typically prioritize this system to keep their business clients confident in platform security.

Together, these seven systems cover the fraud cycle end-to-end, from onboarding to transactions to customer conversations. Most financial institutions deploy a combination, tailored to their biggest risks. And the key is rolling them out without disrupting daily operations, which is where implementation best practices come in.

Implementation Best Practices

Having the right fraud detection systems is one thing. Getting them live in your bank without disrupting daily operations is another. Most institutions underestimate the planning, integration, and monitoring work required. Here’s how to make sure the rollout sticks:

Planning and Preparation

A strong rollout starts long before the first line of code goes live. Banks that succeed usually set expectations up front about budgets, team structure, and timelines:

- Budgeting by Size of Institution: Smaller community banks often spend $50K–$150K on initial deployment. Regional banks typically see ranges of $150K–$350K, while large enterprises budget upwards of $500K when integrating multiple systems across geographies.

- Realistic Timelines: A full rollout usually takes 3–6 months, depending on how many fraud systems you’re integrating. That includes testing, tuning, and staff training.

- Team Setup: You’ll need 3–5 technical staff (data engineers, ML specialists), a dedicated project manager, and at least 2–3 fraud analysts to fine-tune detection models. At Aloa, we can also extend our in-house teams to work with you. This support ensures projects don’t stall from a lack of expertise or bandwidth.

- Legacy Assessment: Map out which systems can connect via APIs and which may need middleware. This prevents last-minute surprises during integration of new data sources.

- Compliance Groundwork: Set up frameworks for AML and KYC reporting ahead of deployment. That way, regulatory reporting doesn’t stall go-live.

Integration Strategy

Even the best fraud detection system will fail without an integration plan. Smooth integration works best in phases, with gradual adoption and plenty of testing. A typical roadmap looks like this:

- Phase 1 - Foundation (Weeks 1–4): Build data pipelines, connect APIs, and establish baseline performance metrics.

- Phase 2 - Intelligence (Weeks 5–8): Train machine learning models and calibrate for your institution’s transaction patterns.

- Phase 3 - Validation (Weeks 9–10): Test against live data, tune false positive thresholds, and optimize for speed.

- Phase 4 - Deployment (Weeks 11–12): Roll out gradually, monitor closely, and integrate feedback from fraud teams.

Working with an experienced partner can ease this process. At Aloa, our AI development specialists use pre-built integration frameworks to cut 40–60% of common rollout issues, making timelines more predictable and reducing risk.

Performance Monitoring

Going live is the start of continuous tuning. The best banks track performance with clear KPIs and keep refining models as fraud patterns change. Some benchmarks worth following are:

- Detection Accuracy: Aim for 95%+ as a baseline.

- False Positives: Keep them under 2%; otherwise, customer frustration will spike.

- Processing Speed: Transactions should be scored in under 100ms to feel real-time.

- Cost per Detection: Target less than $0.50 per flagged event for operational efficiency.

From there, add layers like continuous learning. As fraudsters change tactics, feedback loops can allow models to retrain automatically using machine learning. ROI tracking helps measure avoided financial losses against system costs.

Banks that monitor only surface metrics, like “number of alerts generated,” tend to miss underlying issues. The smarter play is to track detection quality, efficiency, and compliance altogether.

Regulatory Compliance and Security Considerations

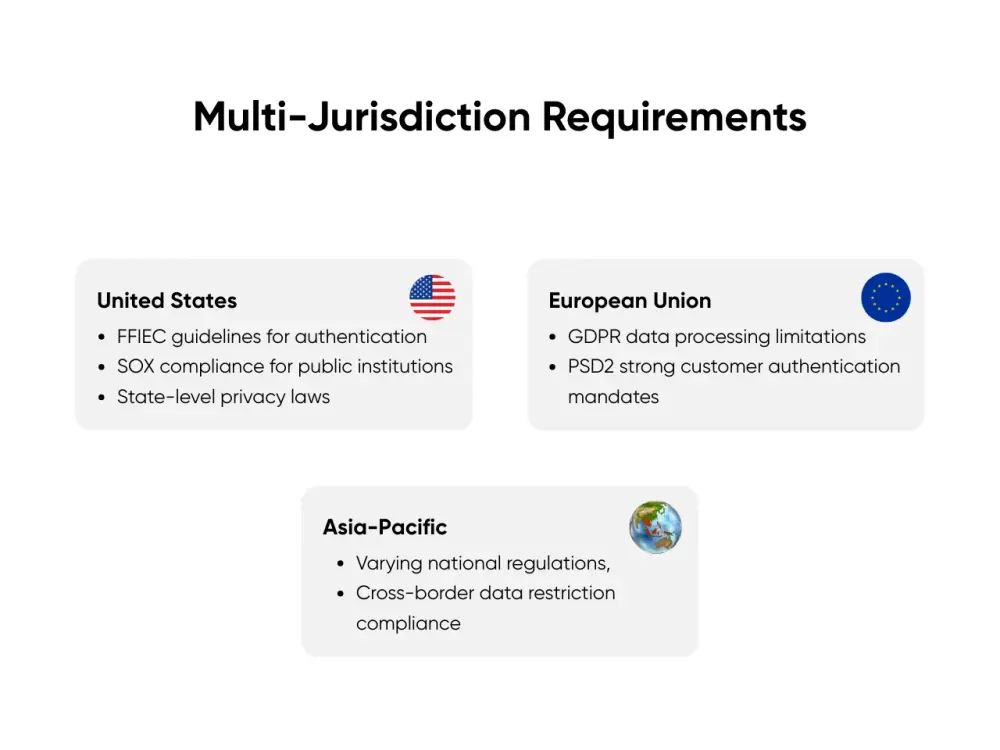

Fraud detection isn’t just about catching bad transactions. It also involves proving to regulators that your systems are airtight. Compliance looks different depending on where you operate, and banks that scale internationally feel this pressure the most.

Here’s what the landscape looks like:

- United States: Banks answer to FFIEC guidelines on authentication, SOX rules for public companies, and a patchwork of state privacy laws. Missing any of these means heavy penalties.

- European Union: GDPR restricts how personal data is stored and shared, while PSD2 requires strong multi-factor authentication for payments.

- Asia-Pacific: Each market has its own banking standards, with strict rules on cross-border data transfers.

To keep pace, modern fraud prevention tools bake compliance into their design:

- Data protection features anonymize personal information during analysis, which cuts exposure risk.

- Automated retention and deletion policies ensure customer data doesn’t outlive its regulatory window.

- Audit-ready reporting means AML, KYC, and suspicious activity reports (SARs) are generated automatically instead of being pieced together by staff or traditional methods.

Security certifications are another baseline. Systems built to standards like PCI DSS for payments, ISO 27001 for information security, and SOC 2 Type II for controls give both regulators and customers confidence.

The payoff is twofold: fewer regulatory headaches and smoother audits, plus customer trust that sensitive data is handled responsibly. For banks juggling multiple regions, compliance isn’t a box to tick. It’s a daily safeguard that protects your ability to operate.

Key Takeaways

Fraud detection is about protecting trust, keeping regulators satisfied, and making sure your systems can withstand the next wave of attacks. Rule-based tools simply don’t offer that level of defense anymore. Real-time fraud detection in the banking sector has become the standard for staying secure and competitive.

Banks that are moving ahead are already investing in AI-driven defenses that learn from every transaction. While rolling these systems out takes extensive planning, it needs to be done with the right partner. At Aloa, we help banks phase in tools, automate compliance reporting, and track the KPIs that matter. If you’re weighing which approach fits your needs best, a consultation can clarify the smartest path forward.

The decisions you make now will shape your tomorrow. And the choice is straightforward: continue patching legacy systems or build fraud defenses that will work in the future. Reach out to Aloa to get started on taking the safer path. We’ll help you roll out fraud detection that connects with your existing platforms, meets compliance requirements, and delivers ROI.