![9 Powerful Applications of AI in Finance [Real-World Examples]](https://cdn.sanity.io/images/sr38gnla/production/cb6e1a5bd5adf6cedbf67fa3428f8b730b14a502-1300x681.webp?w=1200&fm=webp&q=80)

Spending on artificial intelligence in the financial sector is set to climb from $17.7 billion in 2025 to $73.9 billion by 2033. With 85% of institutions already deploying AI, it’s clear that the technology has become a cornerstone of the industry, tackling slow credit approvals, rising fraud, and overloaded service teams.

At Aloa, we help finance teams transition from pilot to production without overburdening their personnel. We start with small, measurable builds that integrate with existing CRM, ERP, or core banking systems, and only expand once the foundation is stable. That way, you see progress you can trust and a rollout your team can manage.

To support your journey, we've compiled this list for you. It covers real-world applications of AI in finance across customer experience, risk, and trading. You’ll also see governance guardrails and change management tactics in order to take steady steps forward.

Understanding AI’s Role in Modern Finance

AI in finance runs credit scoring, fraud screening, algorithmic trading, portfolio rebalancing, compliance checks, and customer support. It spots patterns and makes real-time predictions, cutting manual steps and speeding decisions so teams respond faster to markets and customers. These applications of AI in finance seamlessly integrate into daily workflows, easing pressure on teams and ensuring operations run smoothly.

What AI Brings to Your Business

AI proves its worth when it fixes the bottlenecks your team wrestles with every day:

- Credit Approvals: Automate routine credit decisions and shrink a 48-hour process to under 30 minutes. J.P. Morgan, for instance, cut transaction rejections by ~20% after putting in AI-assisted underwriting and document checks.

- Fraud Checks: Apply anomaly detection and deep learning to strengthen your fraud detection efforts in real time while reducing false positives by 20–30%.

- Customer Service: Deploy chatbots that resolve balance inquiries and password resets to free live agents for mortgage questions or disputes.

- Compliance: Automate monitoring with stronger security measures and audit trails that adapt to regulatory changes.

Financial institutions investing here report shorter time-to-yes for lending, measurable drops in fraud loss rates, and lower compliance spend, all without adding headcount.

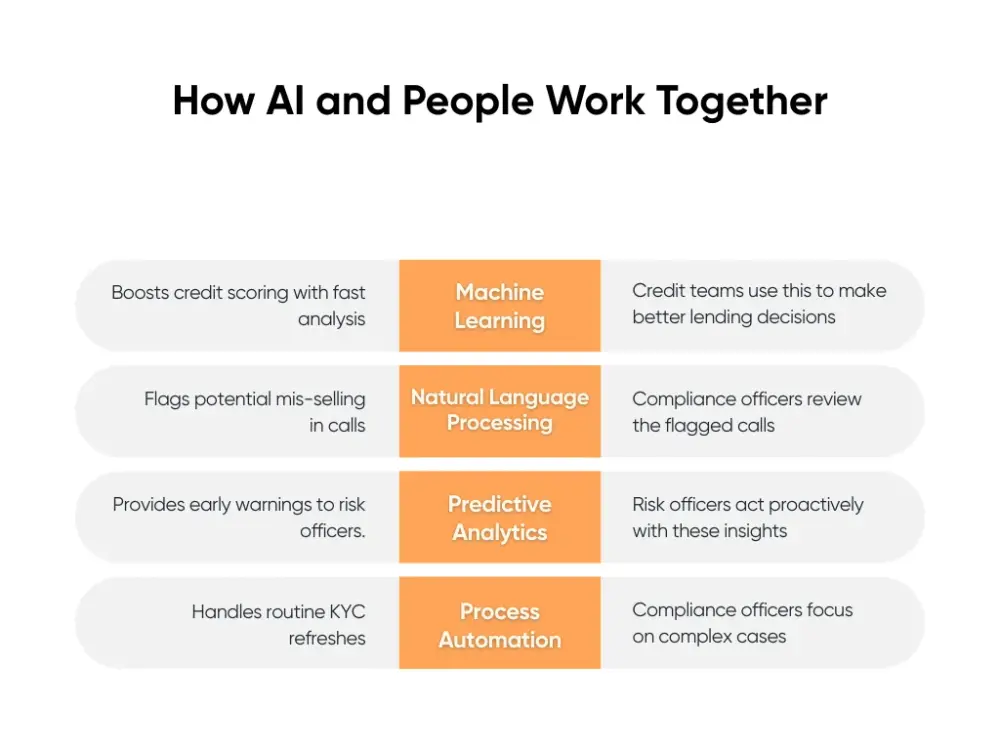

How AI and People Work Together

AI isn’t there to take judgment away from your team. It’s there to scale what they already do best. For example:

- Machine learning strengthens credit scoring by analyzing millions of past applications in seconds.

- Natural language processing reviews call transcripts to flag potential mis-selling or policy gaps.

- Predictive analytics reads market conditions and improves accurate predictions, giving risk officers days of lead time instead of reacting after the fact.

- Process automation pushes routine KYC refreshes straight through, while edge cases go to compliance officers.

Customers respond better when they know there’s human oversight. Cornell University and Tearsheet have covered field experiments showing people trust recommendations more when a human has final say, even in automated investment advice.

For example, fraud detection platforms now block fraudulent card payments in under 50 milliseconds, but flagged cases still route to analysts for review before accounts are closed. This balance keeps decisions accurate, defensible, and regulator-ready.

Concerns You’ll Want to Tackle Early

Here are some of the biggest rollout issues and ways to avoid them:

- Messy data leads to unreliable models: Set ownership and contracts early so everyone knows which data is used and how it’s maintained.

- Fragile integrations can cause outages: Test new models in a sandbox before wiring them into core banking or trading systems.

- Opaque models create audit headaches: Work with vendors that provide clear logs of inputs, outputs, and decision reasons.

Ignoring those basics has costs. Misclassifying credit risk causes higher default rates, and failing audits leads not just to fines but to loss of customer trust. Teams that get those correct first see smoother adoption.

In fact, asset managers that invested in cleaner data pipelines now run AI-driven portfolio construction, with 91% reporting usage or active plans by 2025 (up from 55% in 2023). They start small, measure KPIs like default-rate lift or fraud-catch percentage, and expand only when governance is working as intended.

From there, the natural starting point is customer experience. Chatbots, personalization, and analytics deliver results your clients notice right away. And they’re often the quickest pilots to prove value. Let’s look at those first.

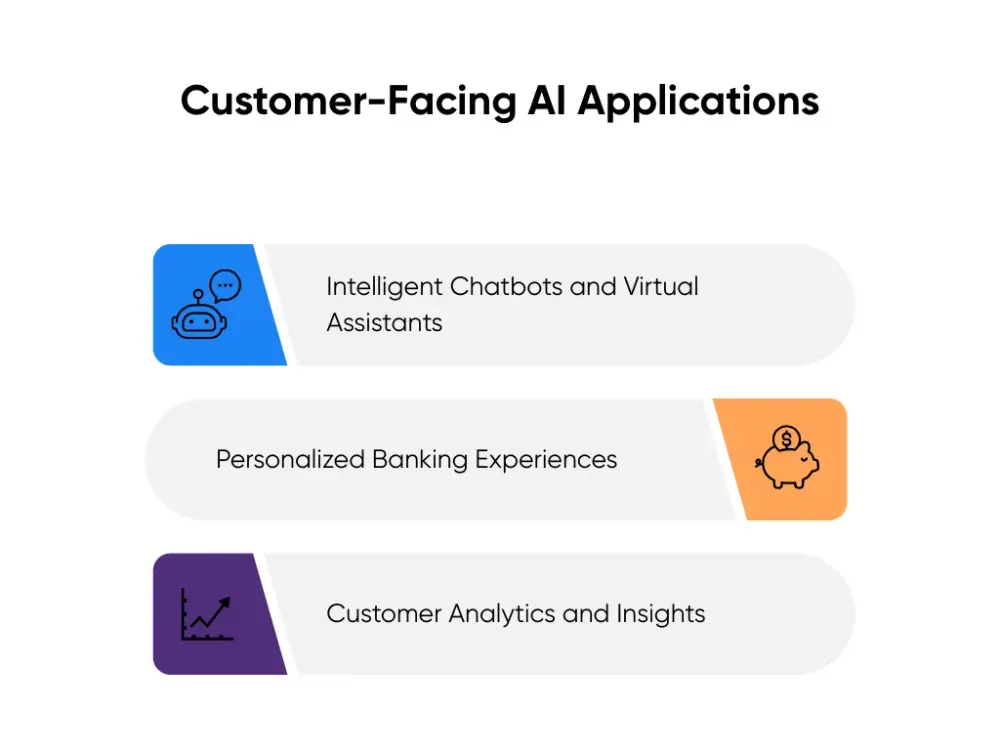

Customer-Facing AI Applications

Customer-facing applications are the parts of AI your clients interact with directly. They handle service requests, give personalized offers, and provide your team with customer behavior insights. Because the impact is immediate, these are often the quickest to prove value.

1. Intelligent Chatbots and Virtual Assistants

Chatbots and virtual assistants can handle routine customer requests (like password resets, balance checks, or card freezes) through mobile apps, web, or voice channels.

Most banks begin by automating the requests that come up most often, such as:

- Identify the 20–30 questions that drive the bulk of call volume.

- Train the bot with large language models fine-tuned on real transcripts so it can confidently handle routine questions like savings account queries.

- Connect it to CRM and core systems so answers stay accurate.

- Define escalation rules so tougher cases hand off smoothly to agents.

- Launch in one channel first and expand only once results are stable.

And the results can be substantial. Bank of America’s Erica serves nearly 50 million users and processes about 58 million interactions each month. Most queries resolve in under a minute, and the internal version halved IT help-desk calls.

2. Personalized Banking Experiences

Personalized banking uses AI to tailor messages, offers, and alerts to each customer. To make this work in practice, banks would:

- Combine transaction, app, and service data into unified profiles.

- Build signals such as churn risk, spending shifts, or account tenure.

- Apply models that rank which message or offer is most relevant.

- Trigger alerts in real time, like a savings prompt after a salary deposit.

- Put safeguards in place, such as frequency caps, fairness tests, and opt-outs.

At scale, personalization has proven to have a significant impact. Bank of America has delivered more than 1.7 billion proactive insights through Erica, from savings nudges to fraud alerts. Customers act on these because the timing feels natural.

The real signals to watch are opt-outs. They’ll tell you if your nudges are becoming too pushy.

3. Customer Analytics and Insights

Customer analytics utilizes AI to analyze transaction records, service logs, and interaction data, surfacing valuable insights. Financial institutions often use it to predict churn or identify high-value clients.

Here's how it's often used:

- Use churn prediction models to flag accounts at risk and trigger save offers.

- Score customer lifetime value (CLV) to help managers prioritize relationships.

- Run RFM and cohort analysis to refine loyalty programs.

- Apply text and voice analytics to uncover compliance risks and recurring pain points.

To take a step further, once you have the analysis, build a dashboard for your team so they can see and interact with the business intelligence where they work. When insights show up in the tools managers already use, they will be able to spot where customers drive the most value and catch gaps if any.

For most financial institutions, this translates to fewer lost accounts, stronger lifetime value, and smarter use of support resources, before shifting focus to larger plays like fraud and risk management.

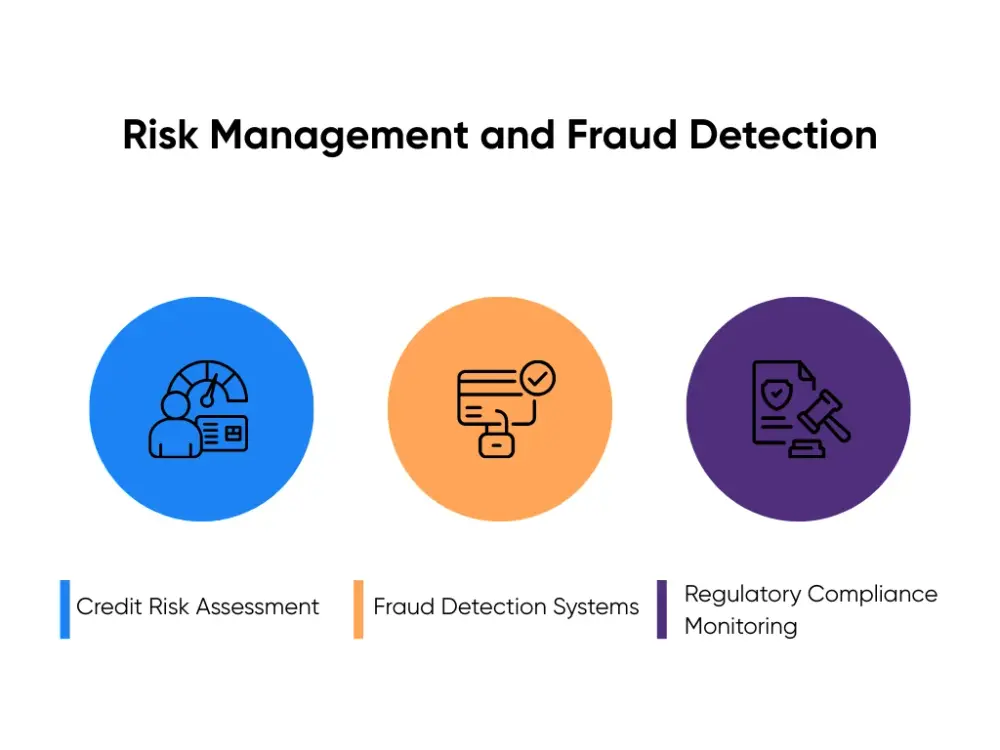

Risk Management and Fraud Detection

Customer-facing tools are an important touch-point with your customers, while risk and fraud systems will protect the business itself. Here, AI enhances credit scoring accuracy, detects fraud in real-time, and provides compliance teams with audit trails. In short, AI simply enhances your existing business functions and enables your team to move more efficiently.

4. Credit Risk Assessment

AI-driven credit risk models go beyond bureau scores. They use data science across big data: repayment history, transaction patterns, and even nontraditional signals like utility payments or rent. The goal is to approve more qualified borrowers, reduce defaults, and cut decision times from days to minutes.

When teams put this in motion, they tend to:

- Consolidate loan and repayment data into one system of record.

- Add alternative data sources to fill blind spots.

- Train machine learning models to predict default risk with explanations built in for regulators.

- Test models on lower-risk products before rolling them out widely.

Some lenders report that approval rates have climbed by 15% without an increase in defaults after adopting machine learning models. Others highlight time-to-yes shrinking from two days to under an hour.

If you’re leading this, watch default rates first, then approval speed and approval volume. When you see more qualified borrowers getting through faster without extra risk, you’ll know the model is paying off.

5. Fraud Detection Systems

Real-time fraud detection platforms scan every transaction as it happens, using AI to flag anomalies like mule accounts, odd spending spikes, or logins from unusual devices. Unlike rules-based systems, these can adapt as fraud tactics shift.

Here are a few key steps you can take:

- Train models on both fraud and clean transaction data.

- Apply anomaly detection and network analysis to uncover suspicious patterns.

- Run models against historical data before switching to live streams.

- Tier the response; let safe payments through, block clear fraud, and escalate uncertain cases to analysts.

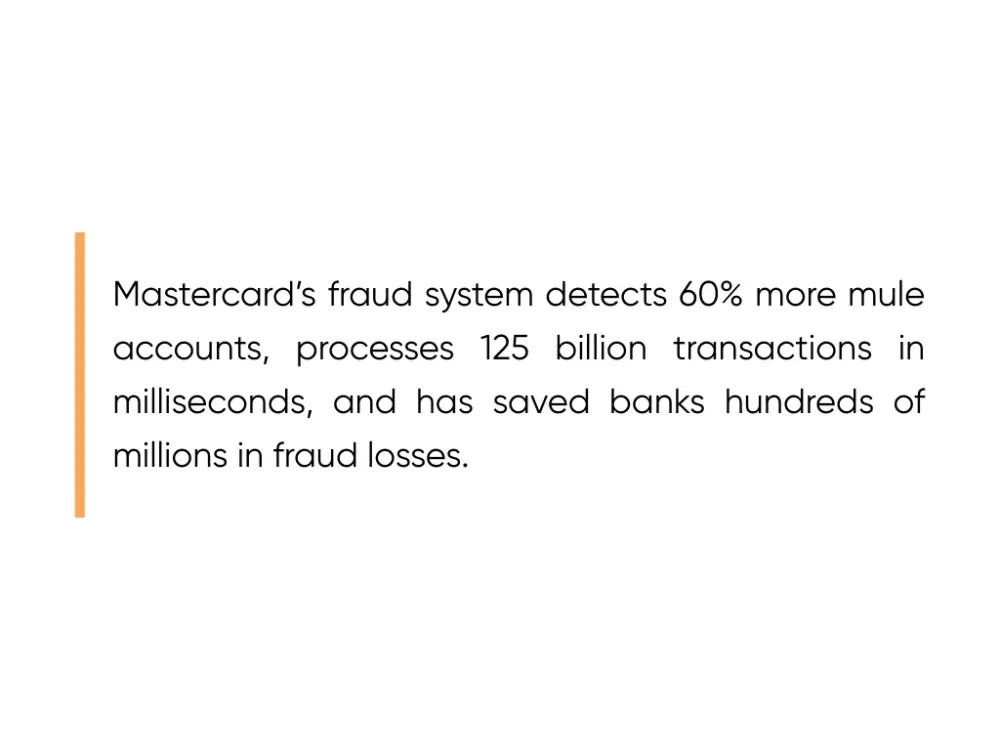

Mastercard’s Consumer Fraud Risk system, for example, has boosted detection of mule accounts by 60% while processing 125 billion transactions a year in milliseconds. Banks using it have cut fraud losses by hundreds of millions.

The measures that matter here are catch rate, false positives, and fraud losses avoided. If fewer legitimate payments are blocked while fraud losses drop, both your customers and your fraud analysts will thank you.

6. Regulatory Compliance Monitoring

Compliance and AML tools apply AI to millions of daily transactions, surfacing suspicious activity and generating reports regulators can trust. They reduce the avalanche of false alerts while freeing staff for higher-value work.

Rolling this out often looks like:

- Connecting AI systems to monitoring feeds for payments and communications.

- Training models on past suspicious activity reports.

- Starting with one high-risk flow, like cross-border wires, before scaling.

- Updating models regularly as regulations change.

Banks using AI this way report cutting compliance costs by up to 60% while producing cleaner audit logs. Staff also spend less time chasing false alerts, which means more time on investigations that matter.

Here, you want to keep an eye on false alert volumes, average investigation time, and audit findings. If alerts drop, case reviews get faster, and regulators stop flagging gaps, you can be confident the system’s working.

Risk and fraud AI builds the guardrails your business needs. Lower defaults, stronger fraud defenses, and faster compliance checks make day-to-day operations safer and more reliable. Once those are in place, trading and investment come in, where AI shifts from protecting value to creating it.

Trading and Investment Applications

This is where AI gives your trading desks, portfolio teams, and analysts an edge. That means spotting opportunities earlier, cutting execution costs, and rebalancing portfolios before risk gets out of hand.

7. Algorithmic Trading Systems

Algorithmic trading systems use AI to scan financial markets and place trades automatically. They’re designed for speed and precision, executing in milliseconds across equities, FX, or crypto.

If you’re thinking about setting this up, the roadmap usually looks like this:

- Pull together years of historical trade and order book data for training.

- Run strategies in a simulation environment first, stress-testing them against past volatility.

- Plug into an execution platform that supports low-latency trading.

- Put guardrails in place (position caps, stop-loss triggers, circuit breakers) so risk doesn’t spiral.

And the payoff should look like JPMorgan’s LOXM. It's improved trade execution by around 15% on price and timing. In crypto, AI bots now scan fragmented exchanges and move on arbitrage opportunities instantly.

What to measure? Execution speed, slippage, and profitability. If your traders see fewer losses to volatility and tighter spreads on fills, you’ll know the model is earning its keep.

8. Portfolio Management and Optimization

Portfolio optimization tools powered by AI test asset mixes, rebalance automatically, and stress-test portfolios against shocks. The goal is to improve returns without adding risk your team can’t defend.

For mid-market asset managers, this usually means:

- Running thousands of allocation simulations across equities, bonds, and alternatives.

- Automating rebalancing when weights drift or risk tolerance changes.

- Applying stress tests for events like inflation spikes or geopolitical shocks.

- Delivering personalized allocation nudges for clients through apps or dashboards.

The adoption trend here shows 91% of asset managers using or planning to use AI in portfolio construction, up from 55% in 2023. Early adopters report higher Sharpe ratios and fewer drawdowns.

The KPIs you’ll want to put on your dashboard are volatility, Sharpe ratio, and tracking error. If returns hold steady or rise while risk-adjusted performance improves, you’ll have proof points leadership can stand behind.

9. Market Analysis and Prediction

Market analysis platforms read news, filings, earnings calls, and social media. They blend investment research signals that point to the future of finance. And the edge comes from reacting hours (or days) ahead of the market.

A typical workflow involves:

- Using NLP and generative AI to summarize unstructured data from calls and headlines into trader-ready notes.

- Applying sentiment analysis across investor reports, news, and social feeds.

- Training predictive models to forecast price swings or sector shifts.

- Pushing those insights directly into trading and portfolio dashboards where your team works.

Some funds now process billions of data points daily, surfacing signals long before traditional analysis. For example, sentiment dips in social channels have predicted earnings misses days before official releases.

Here, focus on prediction accuracy, lead time, and incremental alpha. If your analysts can position ahead of earnings surprises or sector rotations with confidence, you’ll see the edge show up in your returns.

AI in trading and investment moves you from defense to offense. Instead of just protecting capital, you’re actively creating value with faster trades, smarter portfolios, and earlier signals. But the challenge isn’t proving upside; it’s rolling these out with the governance, data quality, and change management that keep things steady once they scale.

Implementation Roadmap and Best Practices

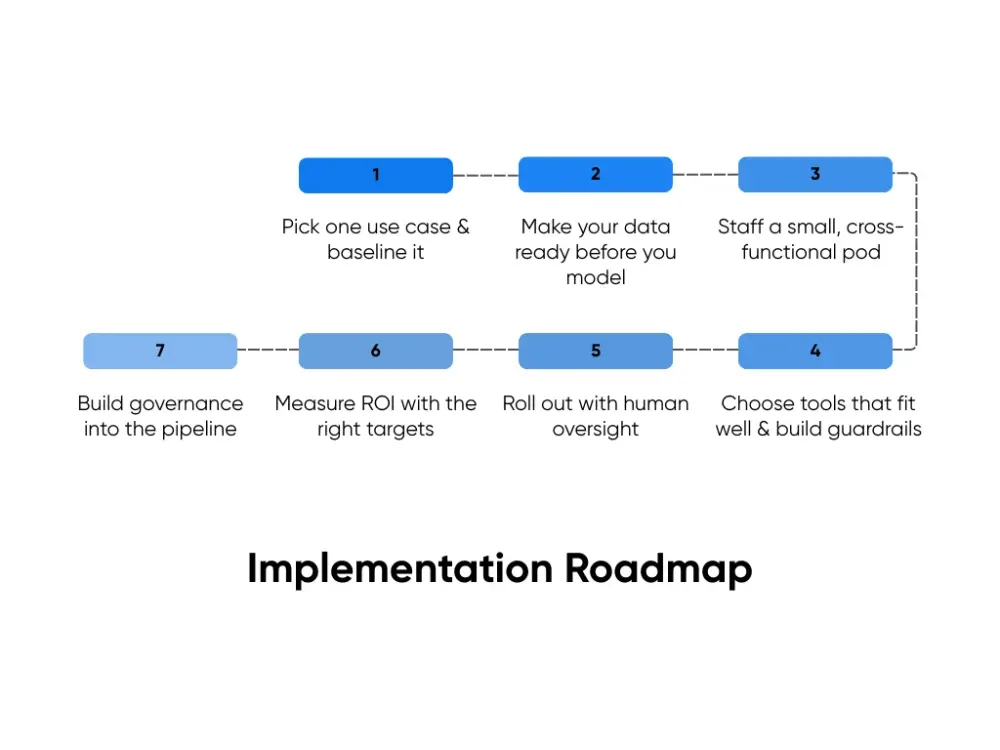

Moving from pilot to production isn’t about bold visions. You need a plan your team can actually run. Here’s a practical roadmap you can use to launch safely, prove value, and scale without breaking your systems:

Pick one use case and baseline it

Start where a win is visible and easy to measure. Credit approvals, fraud checks, customer support, or compliance reporting all work:

- Focus on a single workflow in one channel or product line.

- Capture today’s numbers: time to yes, fraud losses, review time, error rate.

- Define a 90-day goal leadership will notice, like halving approval times.

That focus keeps the first project manageable while showing value quickly.

Make your data ready before you model

Good models fail when data is messy. Tighten the basics first:

- Assign owners and stewards for critical datasets.

- Set contracts for schema, refresh cadence, and quality.

- Apply controls for PII, role-based access, and audit logs.

- Use a model registry and feature store for consistency.

Clean data avoids the trap of shipping a model no one trusts.

Staff a small, cross-functional pod

A lean team is easier to manage and moves faster:

- Core seats: product owner, data engineer, ML engineer, ops partner, compliance lead.

- Define who approves, who builds, and who supports.

- Keep meetings short and ship in weekly cycles.

Having compliance at the table from day one reduces rework later.

Choose tools that fit well and build guardrails

When evaluating tools, look past glossy features and check:

- Certifications like SOC 2 or ISO 27001.

- Explainability features with decision logs.

- Native hooks into CRM, core banking, or warehouses.

- Latency that meets service-level agreements.

- Clear exit plans to avoid lock-in.

The right partner gives you both speed and resilience.

Roll out with human oversight

Don’t trust a model blindly. Design rollout steps with control points:

- Start in shadow mode and compare to current processes.

- Tier responses: approve safe cases, block clear fraud, escalate the grey zone.

- Keep a rollback switch ready for safety.

- Track inputs, outputs, and latency in one dashboard.

- Communicate changes clearly and train staff with short playbooks and refreshers.

This builds trust while adoption grows.

Measure ROI with the right targets

Track outcomes in terms leadership understands:

- Service: 40%+ containment with stable CSAT.

- Fraud: 20–30% fewer false positives, lower fraud losses.

- Credit: Approvals in minutes with stable or lower default rates.

- Compliance: 25–40% fewer false alerts, faster reviews, cleaner audits.

- Trading: Lower slippage, stronger Sharpe, tighter tracking error.

Clear metrics turn pilots into defensible business cases.

Build governance into the pipeline

Governance should run alongside delivery, not after:

- Model approvals and versioning.

- Bias and fairness testing before and after launch.

- Drift monitors with alerts for unusual behavior.

- Incident runbooks with clear owners.

- Quarterly reviews with evidence from logs.

This makes scaling safe and regulator-ready.

This roadmap works because it’s built for mid-market teams balancing ambition with stability. You prove value in 90 days, scale only what delivers, and keep governance in the loop from day one. If you’d like a partner to help set up the first pod, integrate into CRM or core banking, and leave your team with playbooks they can own, we can help through Aloa’s finance AI development services.

Key Takeaways

You don’t need all the answers on day one. What you do need is one use case, clean data, and a 90-day window to prove it works. From there, you can scale step by step, with your team in control and the right guardrails in place. That’s how the applications of AI in finance become part of your business instead of another stalled project.

And if you’d rather not figure out the plumbing alone, we’ve done this with finance teams facing the same pressure you are. Book a call with Aloa and let’s design the first build together: small, measurable, and steady enough that everyone can trust it.

FAQs About AI in Finance

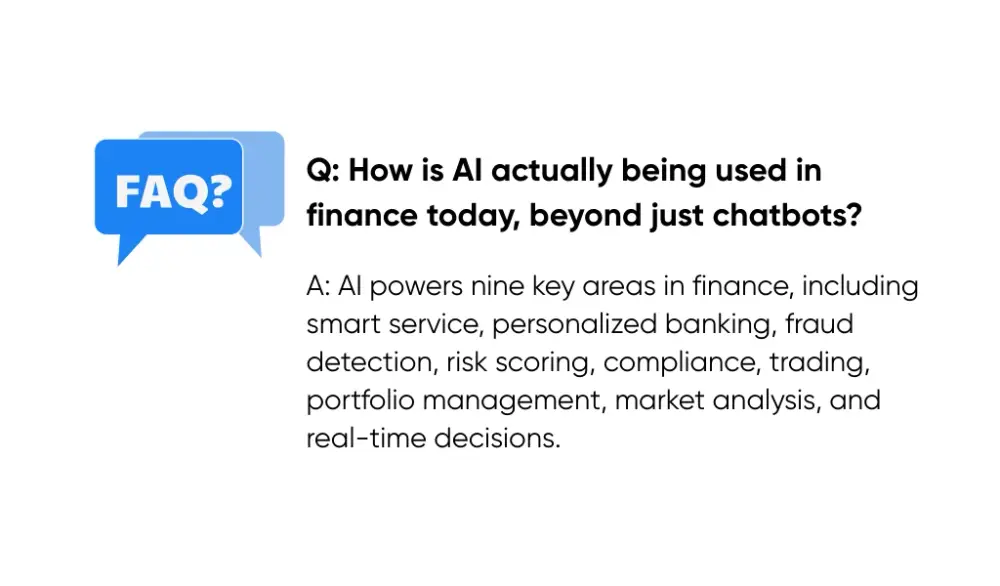

How is AI actually being used in finance today, beyond just chatbots?

It’s not just about answering customer questions. AI now supports nine big areas: intelligent service, personalized banking, fraud detection, credit risk scoring, compliance automation, algorithmic trading, portfolio optimization, market analysis, and real-time decision support. JPMorgan’s COIN reviews contracts in seconds, while Goldman Sachs uses AI models to run trading strategies that generate billions.

How do banks use AI to analyze customer behavior and preferences?

AI reviews transaction patterns to group spending, spot habits, and even predict life events like a home purchase or retirement. Banks use this to segment customers for targeted offers, identify those at risk of leaving, and tune products in real time. That’s how teams make personalization immediate instead of reactive.

What’s required to implement AI-powered customer analytics?

You’ll need clean data stitched together from all touchpoints, a data platform that can handle real-time processing, and machine learning models built on top. Add compliance rules for privacy, training for staff, and tight CRM or marketing integrations. Most projects take 6–12 months and involve both tech and process changes. For support, see our finance development services.

How does AI help with regulatory compliance in finance?

AI automates monitoring by scanning transactions and communications for suspicious activity, generating regulatory reports automatically, and tracking risk exposure in real time. Institutions using these tools report 25–40% lower compliance costs along with faster, more accurate reviews, which makes regulators and auditors a lot more comfortable.

What’s the typical timeline and cost for implementing AI in a financial institution?

Simple chatbots take 2–3 months. Fraud detection or credit risk systems can run 6–12 months. Costs range widely, from around $100,000 for narrow projects to more than $10 million for enterprise-wide programs. Most teams start with pilots in the $50,000–$500,000 range before scaling. To scope yours, explore our finance development services.