Fintech AI is actively being deployed across multiple fintech niches. AI is already transforming core functions in digital banking, payments, lending, and RegTech, providing process automation, advanced data analytics, and more.

At Aloa, we help businesses design and implement custom fintech AI solutions in various fintech niches. We employ a consultative, end-to-end development process that accounts for your unique compliance, operational, and UX requirements. This lets us rapidly validate ideas with prototypes, and smoothly integrate full-scale AI systems with your existing operations.

In this blog, we’ll explore the most impactful trends shaping fintech AI in 2026. We’ll also give you valuable insights on how AI is empowering businesses to meet customer demands and take on evolving challenges in the fintech sector.

Let's dive in!

TL;DR

- One of the most prominent trends across all fintech niches is the increasing use of AI and ML for customer experience, risk management, fraud detection, process automation, and predictive analytics.

- Key niches that fintech AI is transforming include digital banking, robo-advisors, RegTech, and financial record maintenance. Each fintech niche is seeing enhanced personalization, efficiency, and compliance thanks to advanced AI insights and automation.

- Top 2026 trends include the rise of A2A (account-to-account) payments, CBDC (central bank digital currency), AI in anti-money laundering, sustainable fintech, and biometrics in embedded payment services.

- Across all fintech niches, customers are receiving better UX, faster transactions, stronger security, and more precise credit scoring.

What is FinTech AI?

FinTech (sometimes spelled “fintech”) AI is a powerful tool bringing intelligent risk assessment, natural language processing, and other advanced technologies to various fintech niches. Thanks to fintech AI, companies can analyze massive volumes of data, deliver personalized customer experiences, automate repetitive tasks, and boost operational efficiency overall.

These tools also help small business owners keep their business bank account organized by tracking expenses, automating records, and reducing the chances of errors during tax reporting.

One of the significant use cases of FinTech AI is credit scoring, where it evaluates user behavior and historical data to calculate credit scores more accurately. Its capabilities extend to fraud prevention, detecting and mitigating financial fraud attempts in real time, safeguarding customer data, and ensuring the security of financial systems.

FinTech AI aids in portfolio management, tracking market trends, and making informed investment decisions. The use of AI in mobile apps and business processes has become one of the best practices adopted by FinTech providers, harnessing the power of AI to manage large amounts of data and secure financial systems.

A growing demand for Fintech businesses is AI visibility and how their brand is being presented across AI engines when prospective buyers are looking to implement such solutions.

FinTech Niches To Apply AI Technology

FinTech AI integration has ushered in a new era of innovation and efficiency. Various niches within the financial technology sector have harnessed the power of AI to enhance their offerings, revolutionizing how we manage finances.

Let's delve into some of these FinTech niches where the application of AI technology is particularly transformative.

Digital Banking

Traditional financial institutions face formidable competition from emerging players seeking to disrupt the industry. Neobanks, in particular, have gained traction by offering superior interest rates, lower fees, and greater transparency in fund management. AI plays a pivotal role in optimizing customer experiences within digital banking platforms. From personalized financial advice to real-time transaction monitoring, FinTech AI ensures that digital banking remains customer-centric and efficient.

Robo-Advisors

The rise of robo-advisors is notable, especially among Millennials, who value the convenience and accessibility of AI-driven financial counsel. As this generation accumulates wealth, the demand for AI-powered robo-advisors increases. These automated platforms analyze user preferences, risk tolerance, and financial goals to construct and manage investment portfolios. With the ability to adapt to changing market conditions swiftly, robo-advisors provide investors with a hassle-free, data-driven approach to wealth management.

RegTech (Regulatory Technology)

Compliance with regulations and preparing extensive documentation can be daunting and time-consuming, often prone to human error. RegTech is where AI excels in automating compliance processes. FinTech AI systems can swiftly navigate complex regulatory landscapes, ensuring financial institutions comply with the latest rules and standards. This reduces non-compliance risk and significantly cuts administrative overhead, making automated compliance software a wise investment.

Financial Records Maintenance

Managing personal finances requires meticulous tracking of spending, bills, bank accounts, and other assets and liabilities. This is where AI-driven financial records maintenance applications come into play. They provide users with comprehensive insights into their financial health, offering budgeting recommendations and helping individuals make informed financial decisions. These applications leverage AI algorithms to categorize expenses, detect anomalies, and forecast future financial trends, empowering users to achieve their financial goals more effectively.

Top 5 FinTech AI Trends to Follow in 2026

As we look ahead to 2026, the FinTech AI landscape is poised for remarkable advancements. The synergy between financial technology and artificial intelligence continues to reshape the industry. In this dynamic environment, staying informed about the top trends is crucial.

Let's explore the five FinTech AI trends that will command attention and drive innovation in the financial sector throughout 2026.

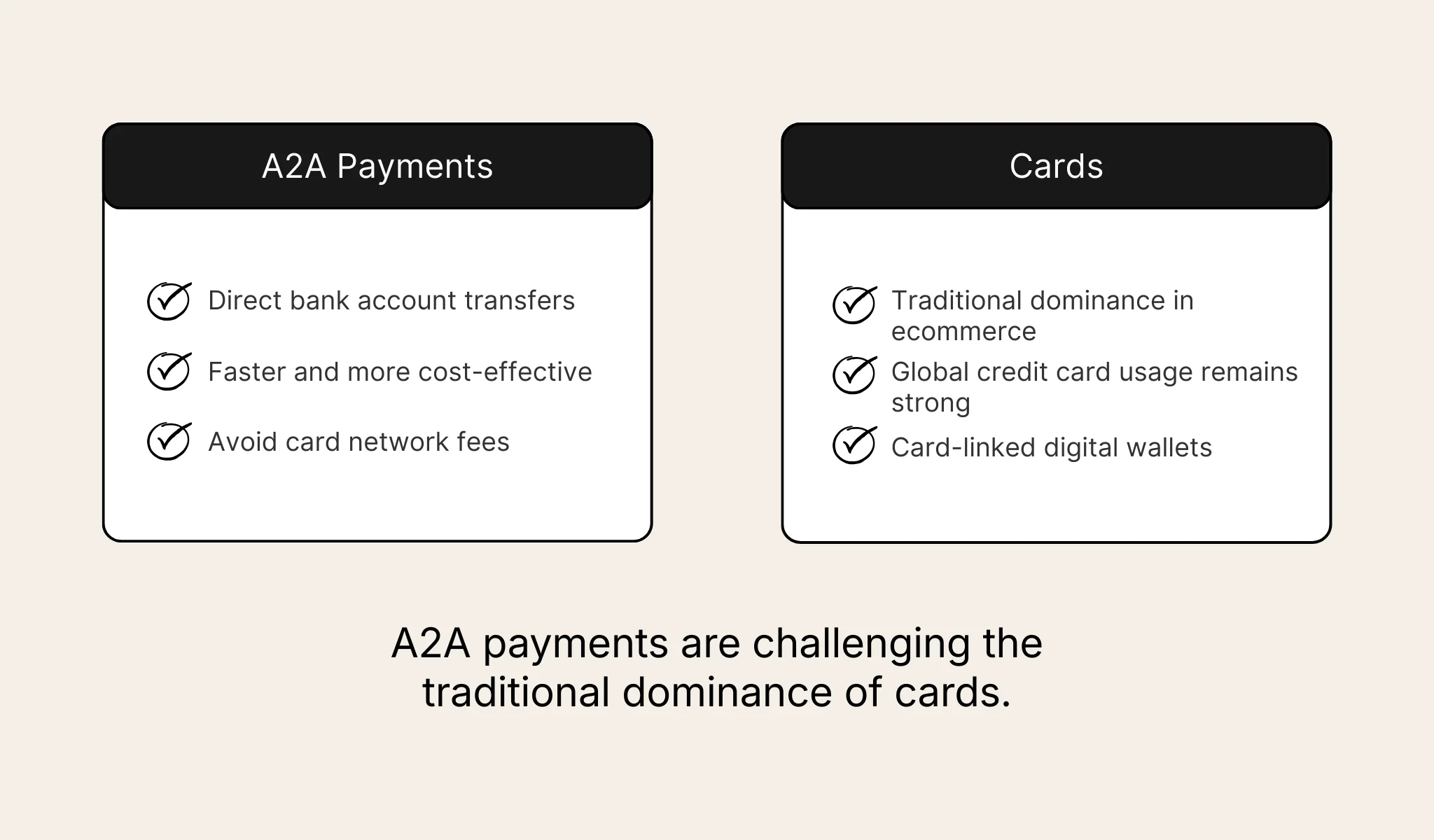

1. A2A Payments vs. Cards in eCommerce & Wallet Funding

A2A (Account-to-Account) payments have emerged as a significant trend in the FinTech industry, challenging the traditional dominance of cards in ecommerce and wallet funding. A2A payments refer to direct transfers of funds from one bank account to another, often facilitated by digital payment platforms. The key drivers behind this trend include the growing demand for faster and more cost-effective payment methods, increased security concerns, and the desire for greater control over financial transactions.

Merchants prefer A2A payments for cost savings and instant settlements, as they avoid card network fees. Despite alternatives gaining popularity, global credit card usage remains strong, with consumers expanding their payment preferences to include card-linked digital wallets and point-of-sale financing options.

Impact of this Trend on the FinTech Industry

This trend is reshaping the FinTech landscape in several ways:

- Lower Transaction Costs: A2A payments typically involve lower fees than card-based transactions. This cost-effectiveness benefits businesses and consumers, making it an attractive choice for eCommerce.

- Enhanced Security: With A2A payments, users have greater control over their financial data, reducing the risk of data breaches and fraud. Enhanced security measures are becoming a priority for FinTech AI developers.

- Streamlined Checkout Processes: A2A payments offer a seamless checkout experience for online shoppers, eliminating the need to enter card details and reducing cart abandonment rates.

- International Transactions: A2A payments facilitate cross-border transactions, providing a global reach for businesses and consumers. This can be especially beneficial in the eCommerce industry, which often operates globally.

- Competition and Innovation: The rise of A2A payments has sparked increased competition among FinTech companies, leading to innovation in payment technologies. This trend encourages the development of more efficient and user-friendly solutions in the FinTech AI sector.

The shift towards A2A payments in eCommerce and wallet funding significantly impacts the FinTech industry by reducing costs, enhancing security, streamlining processes, expanding international capabilities, and fostering competition and innovation.

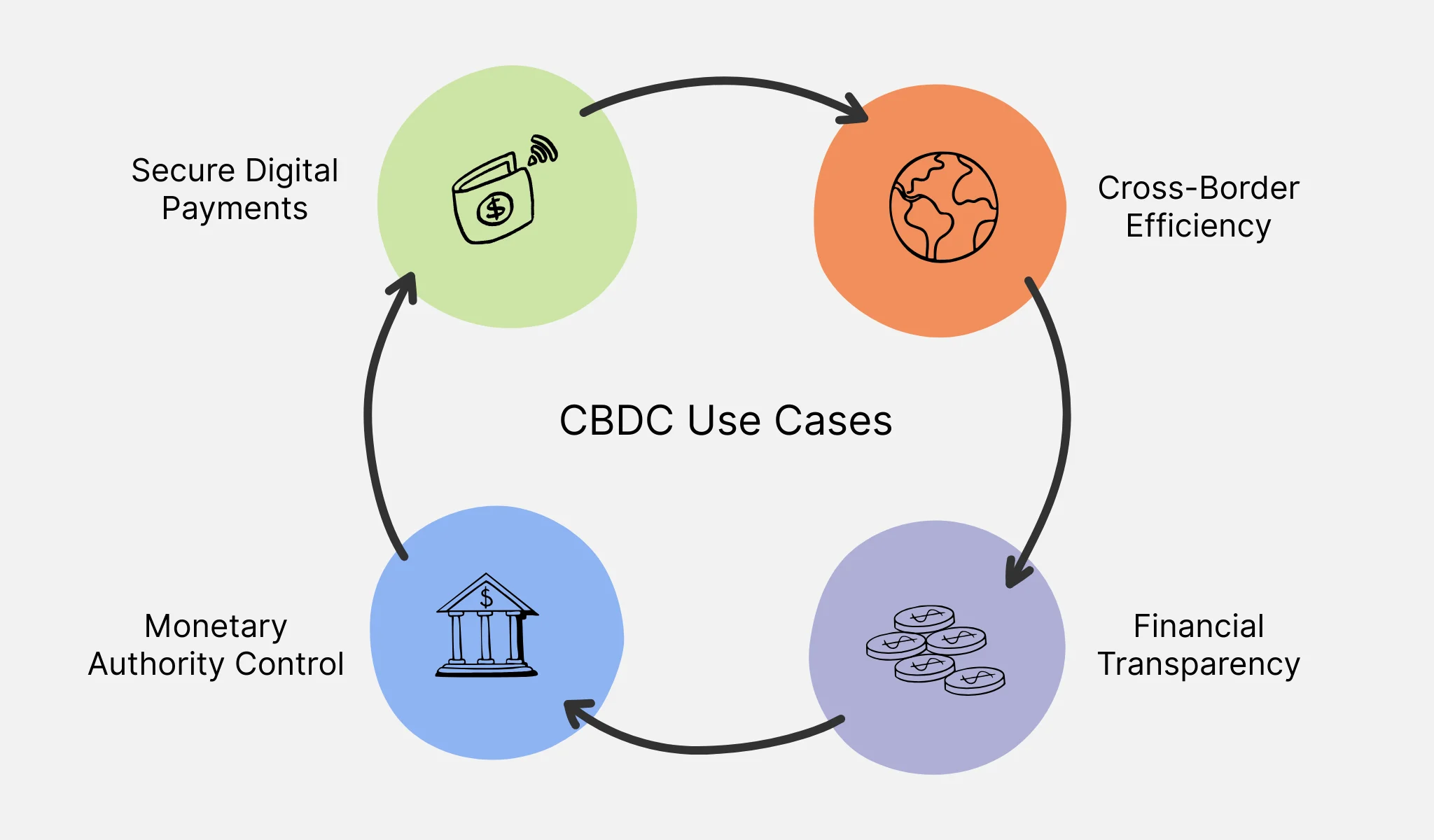

2. CBDC Use Cases Emerging

Central Bank Digital Currencies (CBDCs) have emerged as a groundbreaking development in the financial world. These digital versions of national currencies are issued and regulated by central banks. CBDCs offer a secure and convenient way for individuals and businesses to transact digitally, reducing the reliance on physical cash. They also hold the potential to streamline cross-border payments, reduce transaction costs, and combat illicit financial activities.

In 2022, an event survey showed that Asia-Pacific respondents preferred CBDC and stablecoin use for payments, while EMEA and Americas participants were less specific. This trend emerged as CBDC gained prominence in 2021, contrasting with decentralized cryptocurrencies and stablecoins issued privately. CBDCs, from monetary authorities, represent digital versions of existing currencies. As countries explore the adoption of CBDCs, considerations include technology infrastructure, regulatory frameworks, and privacy concerns.

Impact of this Trend on the FinTech Industry

The emergence of CBDCs is poised to have a profound impact on the FinTech industry, reshaping the financial landscape in several ways:

- Digital Payment Innovation: CBDCs provide a foundation for FinTech companies to create innovative digital payment solutions, enabling faster and more secure transactions for consumers and businesses.

- Financial Inclusion: CBDCs can expand financial inclusion by providing individuals without access to traditional banking services a means to participate in the digital economy, driving FinTech initiatives focused on reaching underserved populations.

- Cross-Border Transactions: The adoption of CBDCs can simplify cross-border transactions, reducing the need for intermediaries and facilitating global trade, a development FinTech firms can harness to provide efficient international payment services.

- Regulatory Compliance: As CBDCs are regulated by central banks, FinTech companies must adapt their operations and technologies to comply with evolving regulatory frameworks, creating opportunities for RegTech solutions.

- Privacy and Security: Developing secure CBDCs will drive the demand for advanced cybersecurity and privacy-focused FinTech solutions as safeguarding digital currencies becomes paramount.

The emergence of CBDCs is set to usher in a new era for the FinTech industry, offering opportunities for innovation, financial inclusion, and improved efficiency while presenting challenges related to regulation and security that FinTech companies must navigate effectively.

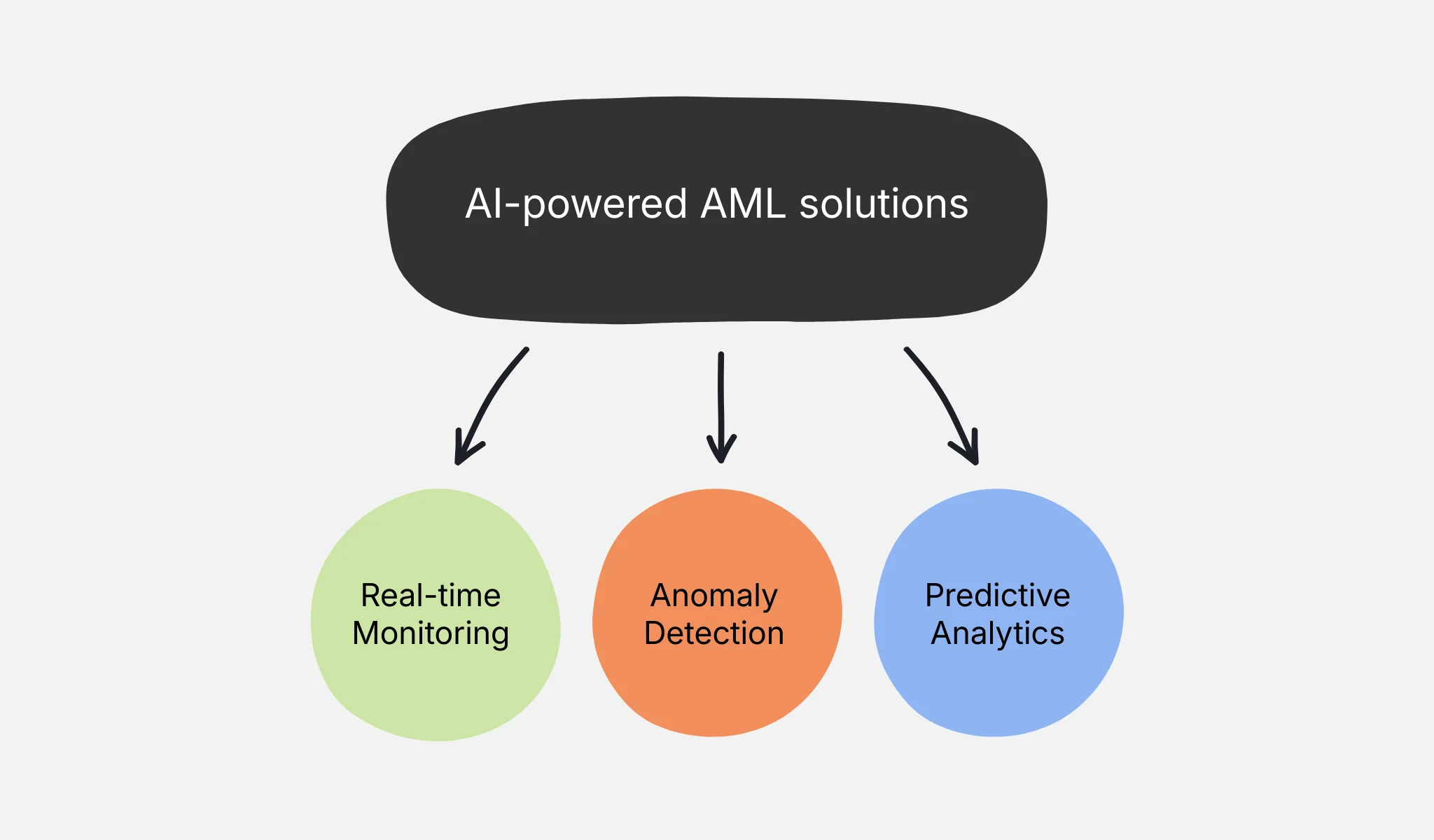

3. AI-Enhanced AML Tools Utilization

AI-enhanced Anti-Money Laundering (AML) tools are gaining substantial traction. These tools are designed to detect and prevent illicit financial activities, a task made increasingly complex by the evolving nature of payment methods and financial transactions. As the financial industry strives to remain compliant with regulatory requirements, AI-powered AML solutions offer real-time monitoring, anomaly detection, and predictive analytics, enhancing the efficiency and accuracy of AML processes.

The IIF and EY Survey Report reveals that over half of banks already use machine learning and 30% run pilot projects. In AML, involving regulators is crucial as they also explore AI adoption.

AI is also applied in document analytics, aiding in fraud prevention. It streamlines processing by extracting vital data from documents like IDs and trade finance papers while flagging discrepancies or potential issues, such as forgery.

Impact of this Trend on the FinTech Industry

Adopting AI-enhanced AML tools is poised to impact the FinTech industry profoundly. Here are five significant ways this trend shapes the landscape:

- Enhanced Risk Management: FinTech companies can better assess and manage risks associated with their services, ensuring compliance with anti-money laundering regulations while maintaining business agility.

- Improved Security: AI-powered AML tools bolster the security of financial transactions, protecting customer data and assets from fraudulent activities.

- Operational Efficiency: Automation of AML processes streamlines operations, reducing manual workloads and operational costs.

- Market Expansion: FinTech firms can expand their services to a broader customer base by demonstrating robust AML compliance, attracting more customers and investors.

- Competitive Advantage: Early adopters of AI-enhanced AML tools gain a competitive edge by offering safer and more compliant financial services, fostering trust among customers and partners.

AI-enhanced AML tools are revolutionizing the FinTech industry by providing effective solutions to combat financial crime while improving operational efficiency and competitiveness. This trend aligns with the industry's commitment to staying at the forefront of technological advancements to better serve regulatory requirements and customer needs.

4. Rise of Sustainable FinTech Solutions

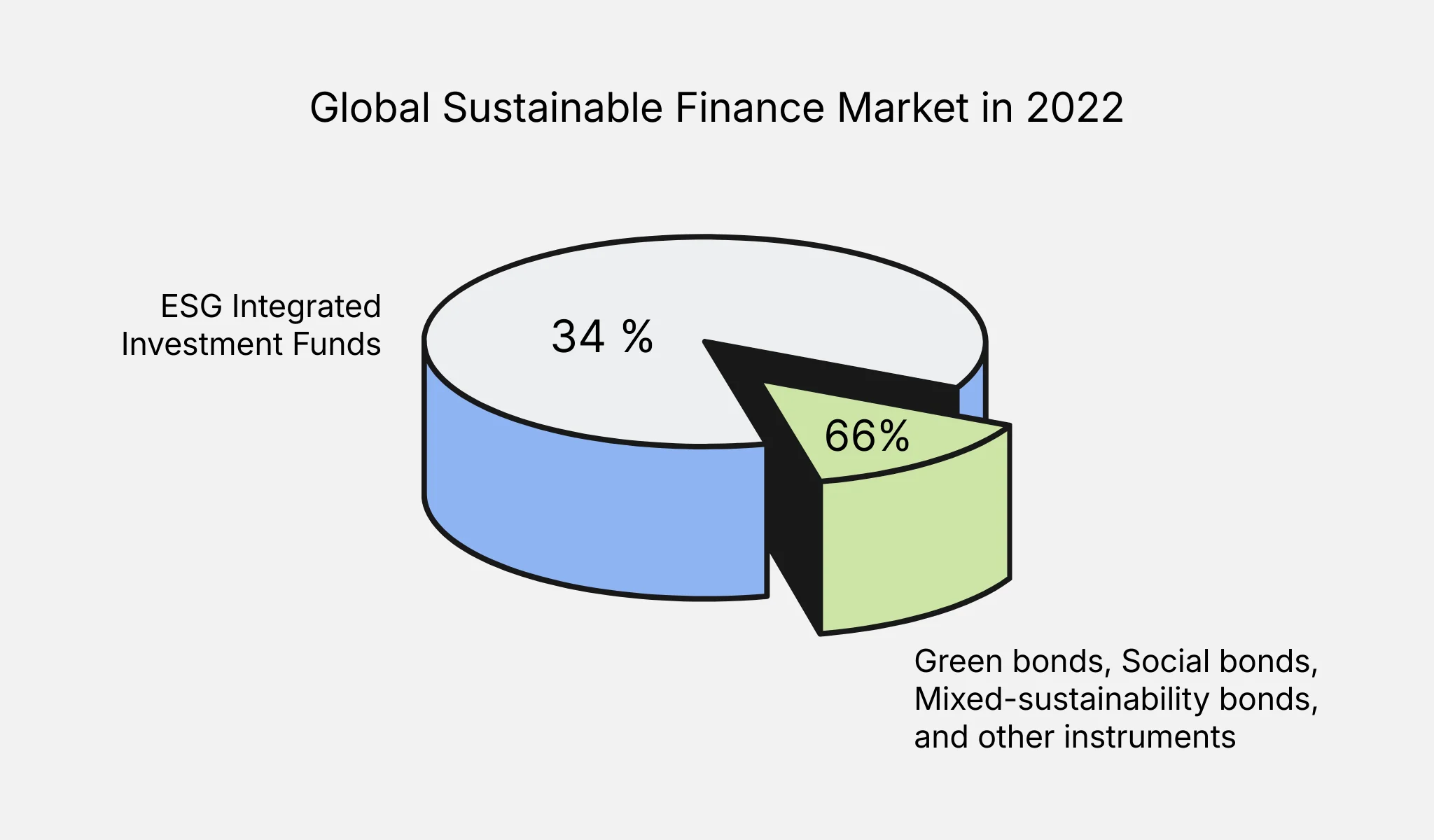

In recent years, FinTech has witnessed the emergence and rapid growth of sustainable FinTech solutions, marked by the integration of environmental, social, and governance (ESG) principles into financial services. The increasing global focus on sustainability drives this trend as businesses and consumers seek more responsible and ethical financial options. Sustainable FinTech solutions encompass a range of offerings, including green investment platforms, sustainable banking services, and eco-friendly payment solutions.

The chart depicts the Global Sustainable Finance Market in 2022, showing a diversified market led by ESG Integrated Investment Funds (34%) followed by Green bonds, Social bonds, Mixed-sustainability bonds, and other categories. This illustrates the rise of sustainable FinTech solutions with various instruments for investors focused on environmental, social, and governance issues.

Impact of this Trend on the FinTech Industry

The rise of sustainable FinTech solutions is reshaping the FinTech landscape in several significant ways:

- Enhanced Investment Choices: Sustainable FinTech platforms provide investors with a broader array of ethical and ESG-focused investment opportunities, empowering them to align their portfolios with their values.

- Improved Risk Management: By incorporating sustainability metrics into financial analysis, these solutions enable better risk assessment and mitigation strategies, reducing exposure to environmentally and socially sensitive assets.

- Eco-Friendly Banking: Sustainable banking services prioritize green lending, reducing carbon footprints, and supporting environmentally friendly initiatives.

- Customer Demand: FinTech firms adopting sustainability principles are attracting a growing customer base concerned with ethical financial practices, fostering loyalty and trust.

- Regulatory Compliance: As regulatory bodies implement stricter ESG reporting requirements, sustainable FinTech solutions help companies navigate compliance challenges and ensure transparency.

The impact of sustainable FinTech drives positive change within the financial industry and contributes to a more sustainable and responsible global economy.

5. Surge in Biometric In-store Payments & Checkout Innovation

The surge in biometric in-store payments and checkout innovation within the FinTech AI landscape represents a remarkable evolution in how consumers interact with financial technology. Biometric in-store payments leverage unique physical attributes like fingerprints, facial recognition, or palm scans to authorize transactions swiftly and securely. Customers no longer need to rely solely on traditional payment cards or cash. Instead, they can complete transactions with a simple touch or glance, significantly enhancing the user experience.

Consumers globally are increasingly adopting biometrics for convenience and security, with 82% of Asia Pacific consumers using an average of three biometric forms. Businesses are also onboard, with biometrics set to authenticate over $3 trillion in payments by 2025.

Impact of this Trend on the FinTech Industry

This surge in biometric in-store payments and checkout innovation is poised to revolutionize the FinTech AI industry in several ways:

- Enhanced Security: Biometric authentication adds a layer of security to financial transactions, reducing the risk of unauthorized access and fraudulent activities.

- Improved User Experience: Customers benefit from faster and more convenient checkout experiences, increasing customer satisfaction and loyalty.

- Reduced Operational Costs: Retailers can streamline their operations by automating and accelerating checkout, potentially reducing staffing needs and costs.

- Data Analytics Opportunities: Biometric data can provide valuable insights into customer behavior and preferences, allowing businesses to tailor their services and offerings more effectively.

- Global Adoption: As biometric technology becomes more widespread and accepted, it will likely be adopted globally, creating a standard for secure and efficient in-store payments.

The surge in biometric in-store payments and checkout innovation indicates the FinTech AI industry's commitment to advancing technology to benefit both businesses and consumers. This trend promises a future where financial transactions are more secure, convenient, and efficient.

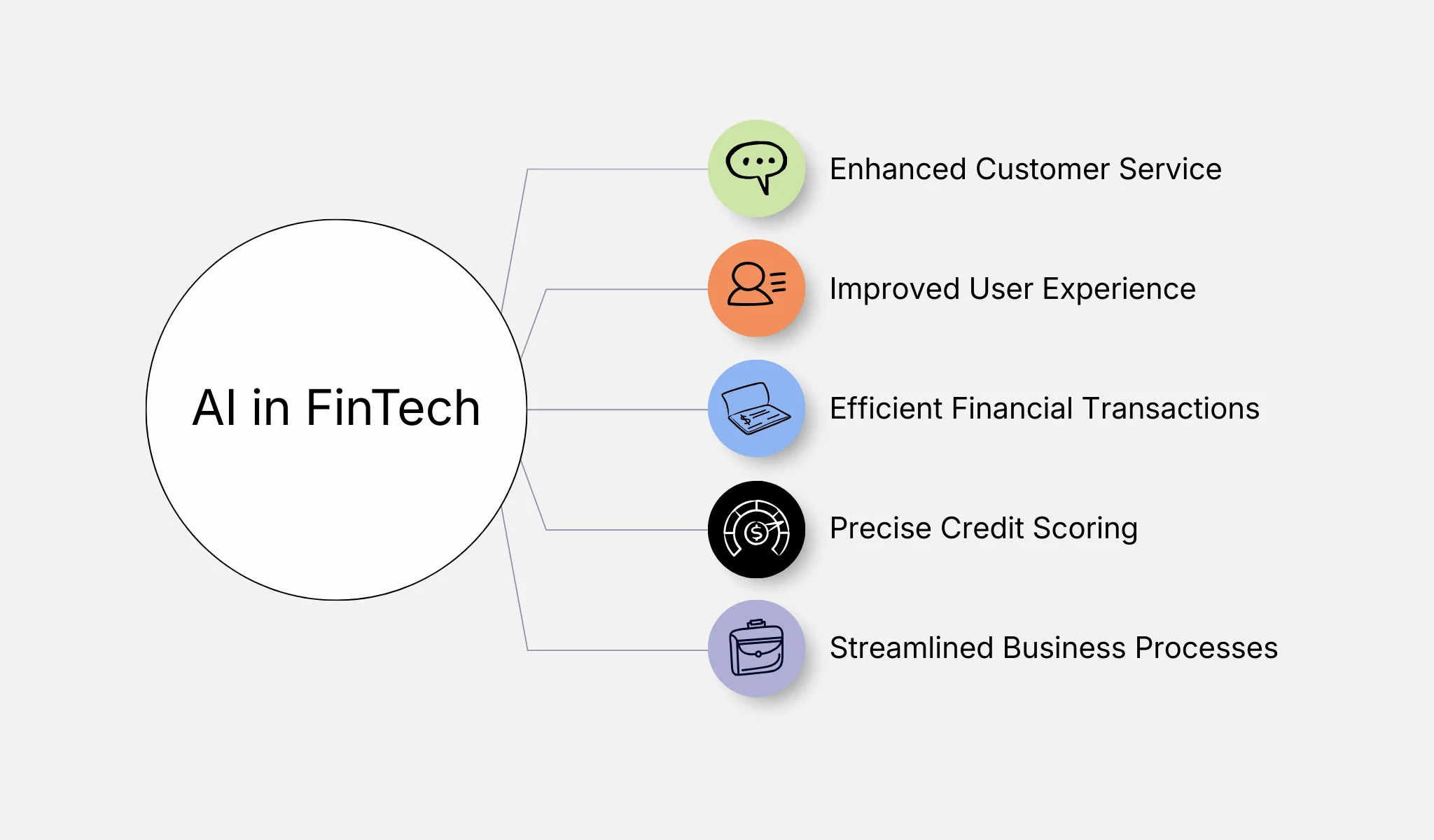

Benefits of AI in FinTech

Artificial Intelligence (AI) has emerged as a transformative force within the financial technology sector. The fusion of advanced AI algorithms with financial processes has paved the way for unparalleled innovation, redefining how we interact with financial services and systems.

Let's explore AI's remarkable benefits to FinTech, showcasing its profound impact on the industry's landscape.

Enhanced Customer Service

One of the primary advantages of incorporating AI into FinTech is the significant enhancement of customer service. AI-powered virtual assistants and chatbots revolutionize how financial companies interact with their clients. These virtual assistants are available 24/7, responding immediately to customer queries, account information, and transaction history. Natural Language Processing (NLP) technology enables these virtual assistants to understand and respond to customer requests, creating a more personalized and efficient experience. This reduces response times and contributes to higher customer satisfaction levels.

Improved User Experience

AI-driven user experience enhancements have become a hallmark of FinTech applications. The ability to analyze user behavior and preferences allows AI systems to provide personalized recommendations, product offerings, and content. For instance, when users access a mobile banking app, AI algorithms can analyze their transaction history to suggest budgeting tips, investment opportunities, or credit card offers tailored to their financial profile. This level of personalization enhances user satisfaction and increases user engagement and loyalty.

Efficient Financial Transactions

AI plays a pivotal role in optimizing financial transactions. AI algorithms can analyze vast amounts of data in real-time to detect fraudulent activities and prevent unauthorized transactions. This is especially crucial in today's digital age, where financial fraud is a persistent threat. Moreover, AI-driven solutions expedite the processing of financial transactions, ensuring that payments, transfers, and settlements occur swiftly and accurately.

Precise Credit Scoring

Credit scoring, a fundamental aspect of the financial industry, has greatly benefited from AI. Traditional credit scoring models rely on historical data and predetermined criteria, which can be limiting. Conversely, AI leverages machine learning to analyze a broader range of data, including unconventional data sources such as social media and online behavior. This enables more accurate and dynamic credit assessments. As a result, AI-driven credit scoring models give financial institutions a better understanding of an individual's creditworthiness, allowing for fairer lending decisions and reduced default risks.

Streamlined Business Processes

In addition to improving customer-facing aspects, AI streamlines various internal business processes within the financial industry. For example, AI-driven Robotic Process Automation (RPA) can handle repetitive, rule-based tasks such as data entry, document verification, and compliance checks. By automating these tasks, financial companies can reduce operational costs, minimize errors, and allocate their human workforce to more complex and strategic functions. This increases operational efficiency and frees up resources for innovation and growth.

Key Takeaway

Many of the fintech AI trends that were still being proven just a few years ago are already transforming multiple fintech niches, and ultimately, how we use fintech products in our daily lives.

Automation and data analytics are now a normal part of fintech workflows. More complex use cases like RegTech, fraud prevention, and personalization are becoming a lot more efficient and accurate. All of this is thanks to real-time AI decision-making and smarter machine learning models that continuously learn from new data.

If you’re looking to integrate AI into your fintech platform, Aloa can be your partner. We design, build, and scale intelligent fintech solutions tailored to your needs and workflows. Talk to us about your AI roadmap today.

If you’d like to learn more, check out other fintech articles on our blog, or join our Discord and exchange ideas with other fintech leaders building with AI. We also have a newsletter: Byte-Sized. Compiled by our co-founder David Pawlan, Byte-Sized brings you the hottest AI news from the past 24 hours, from the latest developments in various fintech niches to healthcare AI and more.

FAQs

How are fintech companies using AI to improve credit scoring?

AI is great at analyzing user behavior, transactional history, and alternative data points to create more nuanced and accurate credit evaluations compared to traditional scoring models. AI also processes large datasets quickly, helping uncover important patterns that traditional models might overlook. This makes risk assessments fairer and more predictive.

What role does AI play in fraud prevention for financial applications?

Instead of static rules like checking whether a customer made a large withdrawal or accessed their account from another country, machine learning models can continuously learn from new activity, detecting subtle anomalies in behavior like unusual timing patterns and small, frequent transactions just under review thresholds.

This subtle anomaly detection is the same way healthcare ML identifies issues like vital sign shifts and patterns in imaging data. At Aloa, we’ve deployed machine learning solutions across various industries. Got a workflow that would benefit from an ML upgrade? Tell us about it.

What are the benefits of using AI for portfolio management in fintech?

AI analytics improves portfolio management by enhancing data-driven decisions. For example:

- Continuous market trend tracking: 24/7 monitoring of global markets can provide instant price movement analysis, news sentiments, and macroeconomic indicator summaries.

- Predictive insights: Machine learning models forecast potential risks and opportunities in asset performance, market volatility, and other trends.

- Automated rebalancing: AI can take the above info to automatically rebalance portfolios to maintain target allocations, helping investors stay aligned with their risk tolerance and long-term goals.

How does AI enhance customer support in fintech applications?

In fintech, customer service AI offers many of the same benefits as it does in other industries. For example:

- Chatbots and virtual assistants: With natural language processing (NLP), fintech chatbots can answer account questions, guide users through transactions, and resolve common issues without human intervention.

- Personalized assistance: AI can analyze customer history and preferences to deliver tailored product recommendations, spending insights, and financial tips.

- Intelligent ticket routing: Machine learning systems can assign priorities to support requests automatically, instantly escalating sensitive issues to the right human agents. It can also direct common queries to existing articles and FAQs to avoid overtaxing your customer service system.

How does AI contribute to operational efficiency in fintech business processes?

AI excels at automating routine tasks. This minimizes human error and accelerates workflows. These benefits by themselves already result in significant cost savings, but for many companies, the real value comes from their teams being freed up to focus on improving the human touch and service quality where it matters the most.